If, then, else: How to choose an IFRS 17 transition approach

22 June 2022

18.2 min read

By Insight.

Problem Statement

The arrival of IFRS 17 is imminent, with insurers required to produce full IFRS 17 financials (including prior year comparative figures) from the 2023 year-end. The IFRS 17 standard describes three possible approaches for calculating the transition balance sheet values for a group of contracts. Many insurers are yet to figure out which of these approaches they need to use for the various groups of contracts within their in-force book.

Group of Insurance Contacts

Entities must identify portfolios of insurance contracts, which comprise contracts subject to similar risks and managed together. Portfolios of insurance contracts issued must be divided into groups of insurance contracts based, at a minimum, on their profitability at initial recognition. Contracts issued more than one year apart in the same group cannot be included in the same group.

Purpose

The purpose of this article is twofold – ultimately to provide a straightforward process for insurers to use when determining the appropriate transition approach to use for their groups of contracts, and initially to explain the IFRS 17 requirements around transition, specifically relating to the approach insurers are required to adopt for calculating the contractual service margin (CSM) and other initial values for a group of insurance contracts.

The information in this article was sourced from three main documents – The International Accounting Standards Board’s IFRS 17 standard (IFRS17), the IFRS 17 basis for conclusions document (BC) and the International Actuarial Association’s document on applying IFRS 17 – International Actuarial Note 100 (IAN100).

Available Approaches

The three approaches described in the IFRS 17 standard are:

The full retrospective approach, which involves measuring each group of contracts as if IFRS 17 had always applied; the modified retrospective approach, which is the same as the fully retrospective approach but with some modifications allowed to fill gaps between the data required and the data available; and the fair value approach, which requires a fair value assessment of the value of the group of contracts.

Only one approach may be used for each group of contracts.

More Detail on the Approaches

1. Full Retrospective Approach

Applying this approach involves measuring each group of contracts as if IFRS 17 had always applied and de-recognising any existing balances that would not exist had IFRS 17 always applied. This requires information from the dates of inception or date of initial recognition, which may be many years before the date of transition to IFRS 17. International Accounting Standard (IAS) 8 requires retrospective application of a new accounting policy, except when it is impracticable to do so. Similarly, IFRS 17 requires a full retrospective application unless doing so would be impracticable.

The assessment of impracticability is to be made per group of insurance contracts.

Impracticable

According to IAS 8 , applying a requirement is impracticable when the entity cannot apply it after making every reasonable effort to do so.

Insurers may consider it impracticable to apply the full retrospective approach where doing so is not possible without the use of hindsight, either making assumptions about what management’s intentions would have been or estimating the amounts recognised, measured or disclosed.

According to IAN100 (12.15), if any of the information required by the full retrospective approach “…is not available or cannot be reasonably estimated, then the full retrospective approach would not be used.” In this context, ‘available information’ means “reasonable and supportable information that is available without undue cost or effort.” (IAN100 12.13)

Reasonable effort versus best effort

If impracticability refers to “every reasonable effort” (as per IAS 8), how does one then define “every reasonable effort”?

Best effort is considered a more onerous requirement than reasonable effort and involves considering every possible thing that can be done and doing everything that could reasonably be done. Something that requires excessive resources to do would not form part of one’s “best effort”, as this could be seen as unreasonable.

Reasonable effort involves doing what is reasonable under the circumstances. This means doing what a reasonable professional person would have done under the same circumstances.

Reasonable effort and best effort have nearly the same meaning – the distinction is that best effort includes the consideration and analysis of every possible course of action, whereas reasonable effort involves pursuing only one course of action, provided it was a reasonable course of action, having regard to the circumstances.

Every reasonable effort would then seem to imply that every possible course of action should be considered, analysed and pursued (within reason). This definition closely matches that of best effort.

Best effort is considered a more onerous requirement than reasonable effort and involves considering every possible thing that can be done and doing everything that could reasonable be done. Reasonable effort involves doing what is reasonable under the circumstances.

Reasonable effort versus best effort

-

-

- Insurers are expected to consider all the possible options for obtaining the data necessary to calculate the initial transition values using the full retrospective approach.

- Each option should then be analysed to determine the cost or effort involved to yield all required data in a usable format.

- If the associated cost/effort required by some options is “reasonable” (or acceptable to the insurer), then it should pursue the easiest or least expensive options and perform the full retrospective approach.

- If an insurer needs to incur significant costs to obtain or convert their data into a usable format, then the full retrospective approach would be deemed impracticable.

-

Unfortunately, the IFRS 17 standard does not specify what significant costs would look like, except that the concept of proportionality should be borne in mind.

This makes the assessment (of whether a full retrospective application would be practicable or not) a judgement call, which would then need to be documented together with the reasons for making the call. These significant judgements must be disclosed.

Demonstrating impracticability

According to IAN100 (12.18), to show that the full retrospective approach is impracticable, an insurer is required “…to demonstrate that, although it has made every reasonable effort to gather the necessary information to enable it to determine required elements retrospectively, that information is either not available OR is available, but not in a form that would enable it to be used without undue cost or effort.”

According to BC378, “…measuring the following amounts needed for retrospective application would often be impracticable:

*notes on the various points

a) the estimates of cash flows at the date of initial recognition;

These expected future cash flow estimates require the best estimate basis at the date of initial recognition, which may not be available.

b) the risk adjustment for non-financial risk at the date of initial recognition;

This often depends on the expected future cash flows at the date of initial recognition, which might not be readily available.

c) the changes in estimates that would have been recognised in profit or loss for each accounting period because they did not relate to future

service, and the extent to which changes in the fulfilment cash flows would have been allocated to the loss component;

This would require every actuarial basis change between the date of initial recognition and the date of initial application.

d) the discount rates at the date of initial recognition; and

Discount rates used in the distant past are unlikely to be available or easily obtainable.

e) the effect of changes in discount rates on estimates of future cash flows for contracts for which changes in financial assumptions have a substantial effect on the amounts paid to policyholders.”

This refers to with-profit business or unit-linked business, where changes in investment return assumptions significantly alter the amounts expected to be paid to policyholders.

The date of initial recognition (for a group of contract) is the beginning of the IFRS 17 coverage period for that group of contracts. This will often be the earliest inception date of all contracts in the group.

The date of initial application is the date that IFRS 17 is applied and has been set as the beginning of the first annual reporting period beginning on or after 1 January 2023. Insurers may decide to apply IFRS 17 earlier than this date.

The date of transition is the beginning of the annual reporting period immediately preceding the date of initial application and for which the insurer presents comparative IFRS 17 information.

Deciding not to apply the full Retrospective Approach

According to IAN100 (12.24), “Simplifications and approximations are allowed when applying the full retrospective approach, if they do not have a material

impact on the results. If any material information is not available and cannot be reasonably estimated, then the full retrospective approach would not be used.”

If an insurer can demonstrate that following the full retrospective approach is impracticable for a group of contracts, then it may choose between the modified retrospective and the fair value approaches. This decision may be based on operational considerations as well as the impact on financial results.

2. Modified retrospective approach

The modified retrospective approach is the same as the full retrospective approach but with some permitted modifications.

The objective of the modified retrospective approach is to achieve the closest outcome to retrospective application possible using reasonable and supportable information available without undue cost or effort.

Examples of permitted modifications for contracts following the General Measurement Model as per IFRS 17 (C8-C19A):

-

- Grouping of insurance contracts can be done using information available at the transition date (or the earliest date for which all the information is available) rather than at initial recognition.

- The need to have separate groups for contracts issued more than one year apart is relaxed in cases where the required information is impracticable to obtain.

- For amounts related to the CSM (or loss component), the cash flows as at the date of initial recognition of a group of contracts may be estimated by the cash flows at the transition date ( or the earliest date for which information is available that will enable the estimated future cash flows at that date to be determined). In other words, ideally, the best estimate actuarial basis at initial recognition should be used. If it is unavailable, then the best estimate basis at the date of transition (or earlier, if available) may be used to calculate the expected future cash flows as the date of initial recognition. For the periods between initial recognition and the date at which future cash flows can be determined, actual historic cash flows may be used. Applying this modification may therefore result in the estimate of future cash flows at initial recognition being a combination of actual cash flows and estimates of future cash flows as at a historical date.

- Discount rates in effect at the date of transition may be used for groups containing contracts issued more than one year apart. Otherwise, if available, the locked-in discount rates are the discount rates that would have been established at the date of initial recognition. If not available, insurers may use the relationship between an observable historic yield curve and the current discount rates to estimate the discount rates as at the date of initial recognition (as outlined in IFRS17(C13)).

- The risk adjustment for non-financial risks at the date of initial recognition can be determined by adjusting the corresponding figure at the transition date by observing the expected release of risk for similar insurance contracts issued by the insurer at the transition date. In other words, the proportion of the risk adjustment remaining at the transition date can be grossed up to estimate the risk adjustment at a contract’s inception date by using a factor consistent with the expected future run-off of the risk adjustment for a similar contract written close to the date of transition.

- Insurers may only use the above and other permitted modifications to the extent that they do not have reasonable and supportable information to apply the full retrospective approach.When applying the modified retrospective approach, insurers need to use reasonable and supportable information and maximise the use of information that would have been used to apply the full retrospective approach, subject to it being available without undue cost or effort.

3. Fair value approach

If a full retrospective calculation is impracticable, then insurers may choose between the modified retrospective approach and the fair value approach.

If an insurer cannot obtain the reasonable and supportable information necessary to apply the modified retrospective approach, then the fair value approach must be used by default.

Under the fair value approach, the CSM or loss component at transition is calculated as the difference between the fair value of a group of insurance contracts at that date (determined in accordance with IFRS 13) and the fulfilment cash flows (present value of best estimate cash flows plus risk adjustment) at that date.

IFRS 13 defines Fair Value as “the price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date.” In the absence of observable market data for insurance liabilities, it is up to the insurer to decide on an appropriate valuation technique to determine the Fair Value.

Cases when the fair value may produce more profitable results than the modified retrospective approach…

The fair value approach may be seen as less onerous to implement because it requires no historical data or retrospective tracking of the CSM. On the other hand, the forward-looking nature and definition of the fair value calculation may result in a differing view of the profitability of that group (such differences are permitted by the IASB). Consider, for example, a guaranteed annuity option which, at some point in the past, has bitten due to an unexpectedly poor period of market performance. The forward-looking fair value CSM may give an unrealistic impression of the group’s overall profitability because it would ignore its performance history. In other cases where groups may be classified as onerous under the full or modified retrospective approaches, there may still be a CSM when the fair value approach is applied. This is because the IRFS 13 fair value measurement indicated that the fair value includes the profit margin that a market participant would require to accept obligations under insurance contacts.

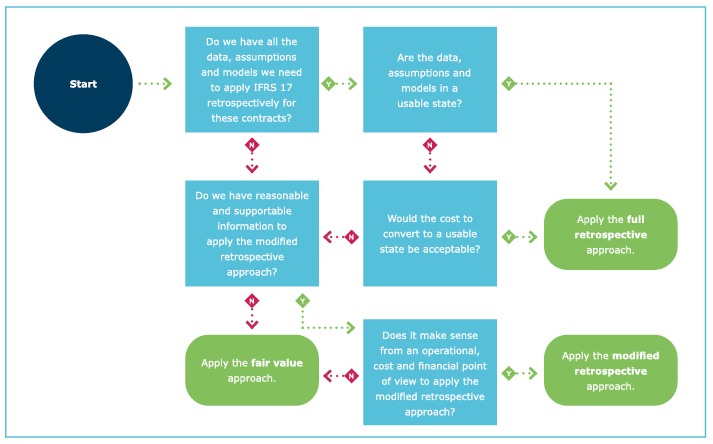

How the decision works

IAN100 (12.14) says that “…the full retrospective approach must be used unless it is impracticable to do so, in which case the entity (insurer) must choose between the modified retrospective approach or the fair value approach.”

For each IFRS 17 group of contracts, insurers should answer the following questions:

- Are all the required historical data, assumptions and models readily available (or easy enough to obtain in a usable format)?

If the answer is “yes”, then perform the full retrospective approach for those contracts.

If “no” then, ask: - Does the insurer have reasonable and supportable information to apply the modified retrospective approach?

If the answer is “no”, then perform the fair value approach for those contracts.

If “yes”, then the insurer is allowed to choose between the modified retrospective approach and the fair value approach and should answer the following question: - Which of the two approaches makes sense from a cost, simplicity and business point of view?

The insurer may then select the more suitable of the two remaining options.

Graphical view of the transition approach decision process for a single group of contracts

The diagram below illustrates the decision process insurers may follow when determining the appropriate transition approach for an IFRS 17 group of contracts.

Next steps

The choice of transition approach is not always a straightforward decision – especially for insurers with long-standing groups of contracts.

The following checklist may provide a starting point for scoping out the activities that need to be performed:

- Perform a gap analysis comparing the information that is available to the information needed to apply the full retrospective approach

- Identify all the possible ways of obtaining the missing information

- Estimate a cost or impact assessment for each of these possible options

- Decide whether any of these options come at an acceptable cost, and, if not, then:

- Compare the practical, operational, business, and financial considerations of selecting either the fair value or modified retrospective approach for each group of contracts for which adopting the full retrospective approach is impracticable.

View or download the PDF here

Insight Life Solutions has a strong team operating in the IFRS 17 space.

Please contact us to discuss the approach that would work best for your business or if you need any other assistance in preparing your IFRS 17 transition balance sheet.

Get an email whenever we publish a new thought piece

In 2023, Insight Life Solutions conducted a series of surveys to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the progress made

3.2 min read

Insight Life Solutions conducted a series of five surveys in Q3 2022 to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the

3.5 min read

Meet our experts

Author

More Insights

Focused Thought Pieces