IFRS 17 asset for insurance acquisition cash flows: Six things to bear in mind

22 August 2022

9 min read

By Insight.

Paragraph 24 says that once groups are established, the entity shall not reassess the composition of the groups subsequently. When considering the allocation of acquisition cash flows to future groups, it should be noted that this requirement does not extend past the contract boundary of any given group. Contract renewals, therefore, are treated as new contracts for the purposes of profitability grouping. Previously profitable policies may, for a number of reasons, become onerous and hence be assigned to loss-making groups upon renewal, and vice versa. A certain profitability status might have been assumed for future renewals (when applying B35A(a)(ii)), but this should be considered a best effort and will be replaced with the actual profitability group when the contract renews.

It may therefore be necessary to revisit the acquisition cash flow allocation based on the movement of contracts between profitability groups. The allocation is only locked in once the group is closed to new business.

Paragraph 28A requires entities to allocate insurance acquisition cash flows to groups of insurance contracts using a systematic and rational method. Once they have been allocated to those groups, paragraph B125 stipulates that the entity must determine insurance revenue (and the same amount as insurance service expenses) related to insurance acquisition cash flows by allocating the portion of the premiums that relates to recovering those cash flows to each reporting period in a systematic way on the basis of the passage of time.

Re(insurers) will therefore need to make two allocation decisions regarding a set of acquisition cash flows: firstly, how to allocate the acquisition expense cash flows to current and future groups and secondly, how to recognise the amount in profit and loss over the coverage period of each group, which may cover multiple years.

It is worth bearing in mind that recovering cash flows on the basis of the passage of time does not necessarily mean assuming uniform recovery over the period. It does, however, preclude approaches that rely on other metrics such as coverage units. It also precludes distinguishing between policies that have been sold versus those that have been renewed in the group. The allocation method does not need to cover the full term of the insurance group, so it is possible to limit recognition to a fixed period of time. The allocation approach between groups (both initial and renewal) has more flexibility allowing for the use of measures such as premium volume or policy count.

When testing for recoverability at the end of each reporting period, impairment tests must be performed for each future group to which the acquisition cash flows have been allocated separately. If the expected net cash inflow of a given group is less than the carrying amount of its related acquisition cash flow asset, the difference is recognised as an impairment loss in profit and loss and in the carrying amount of the asset. If, at some future point, the impairment conditions no longer exist or have improved, the impairment loss must be reversed in profit and loss – this is mandatory, not an option the insurer has. The mantra of ‘but it’s prudent’ will not be accepted here.

Insurers, therefore, need to keep track of the original unimpaired value of the asset to allow for future reversals if necessary.

According to paragraph 28B, a (re)insurer must recognise an asset for the related insurance acquisition cash flows paid or incurred before the recognition of the group. The Standard then says that “[a]n entity shall recognise such an asset for each related group of insurance contracts.”

This means that a separate asset needs to be recognised and maintained for each group. Following this, references to asset impairment (B35D) apply to each asset, rather than having a single acquisition cash flow asset covering all future renewal groups and testing that asset for recoverability. The operational and financial impacts of this distinction should be factored into any planning and decision-making.

Most published examples illustrating the acquisition cash flow allocation assume one-year contract boundaries. But how should incurred acquisition cash flows be allocated to future renewals when the premium guarantee period is longer, say, five years?

In the case of a 5-year guarantee period, acquisition cash flows relating to renewals can only be allocated to groups incepting in five, 10, 15 (or any other multiple of five) years’ time. Here, the structured and organised maintenance of separate acquisition cash flow assets for future IFRS 17 groups mentioned above becomes even more important.

It is also important to remember that the recognition of acquisition cash flows must apply to all policies within a group. So, if a (re)insurer has one group which includes both new policies and renewal policies, the recognition of acquisition cash flows cannot have a separate recognition pattern for the two sets of policies because they are in the same group. Insurers may choose to put new policies and renewal policies into separate IFRS 17 groups because they are managed separately, which would permit different treatments.

When preparing a transition balance sheet, (re)insurers are expected to apply IFRS 17 as though it had always been in force. There is, however, a specific exemption given in C4(aa) which says that (re)insurers do not need to apply the recoverability assessment before the transition date. The impairment test must be performed on the transition date (the beginning of the annual reporting period immediately preceding the date of initial application). This exemption is consistent with the rest of the Standard, particularly 28F, which requires (re)insurers to reverse any impairments that are no longer needed. (Re)insurers who have a material impairment on transition will want to understand the timing of and reason for those impairments to provide a complete explanation for profit recognition under IFRS 17 to management and Boards.

As the implementation date draws nearer, insurers are starting to pay attention to some of the more subtle requirements of the IFRS 17 Standard. With so many elements to keep track of, applying a systematic approach to IFRS 17 implementation is important. Insight Life Solutions has experienced consultants operating in this space – please be in touch should you wish to discuss your IFRS 17 challenges and requirements.

insight.co.za | lifesolutions@insight.co.za [1] IFRS17 B35A(a) [2] IFRS17 B35A(b) [3] IFRS17 28B [4] IFRS17 28C [5] IFRS27 28E

Background

The IFRS 17 Standard makes provision for the allocation of insurance acquisition cash flows to future groups of insurance contracts. Specifically, insurance acquisition cash flows that are directly attributable to groups of insurance contracts need to be allocated to groups of newly issued contracts and any future groups that are expected to arise from expected renewals of the newly issued contracts[1]. Insurance acquisition cash flows not directly attributable to a group of contracts but directly attributable to a portfolio of contracts are allocated to groups of contracts in the portfolio or expected to be in the portfolio[2].

(Re)insurers must recognise as an asset insurance acquisition cash flows paid or incurred before the related group of insurance contracts is recognised[3]. The (re)insurer must then derecognise the asset for insurance acquisition cash flows when the insurance acquisition cash flows are included in the measurement of the related group of insurance contracts[4].

Furthermore, (re)insurers are required to assess the recoverability of the asset at the end of each reporting period if facts and circumstances indicate the asset may be impaired, applying two levels of impairment tests[5], described in B35D. Facts and circumstances should not be misunderstood to mean ‘when conditions are investigated’.

We have summarised six considerations relating to insurance acquisition cash flows which may not be obvious upon first reading of the Standard.

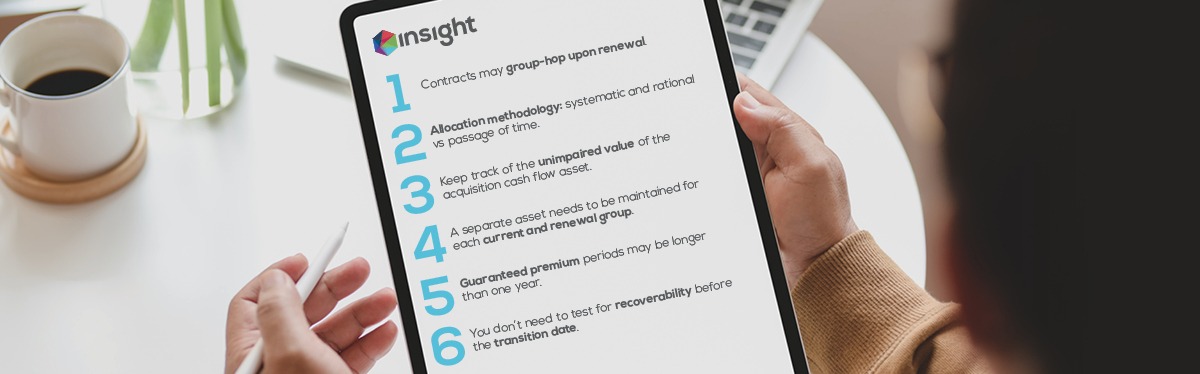

1. Contracts may group-hop upon renewal

2. Allocation methodology: systematic and rational vs passage of time

3. Keep track of the unimpaired value of the acquisition cash flow asset

4. A separate asset needs to be maintained for each current and renewal group

5. Guaranteed premium periods may be longer than one year

6. You don’t need to test for recoverability before the transition date

insight.co.za | lifesolutions@insight.co.za [1] IFRS17 B35A(a) [2] IFRS17 B35A(b) [3] IFRS17 28B [4] IFRS17 28C [5] IFRS27 28E

Get an email whenever we publish a new thought piece

In 2023, Insight Life Solutions conducted a series of surveys to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the progress made

3.2 min read

Insight Life Solutions conducted a series of five surveys in Q3 2022 to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the

3.5 min read

Meet our experts

Author

More Insights

Focused Thought Pieces