IFRS 17: where are South African life insurers?

25 July 2023

7.7 min read

Image by rawpixel.com on Freepik

Industry survey report back

Pamela Hellig, Senior Actuarial Manager

Insight Life Solutions

Insight Life Solutions conducted a series of five surveys from February to May 2023 to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the progress made to date on IFRS 17 implementation and industry thinking – especially in areas where the Standard allows discretion.

A total of 16 entities, comprising traditional insurers, bancassurers and reinsurers, participated in the series, with between 6 and 13 respondents to each survey. A similar series of surveys was conducted in 2022, which meant that inferences could be made, to an extent[1], regarding the progress of the industry over the preceding 12 months.

It is hoped that participants and readers will use the results to benchmark their approach against the rest of the market, as well as against their own future decisions as IFRS 17 implementation matures, discussion around these topics settles, and industry consensus is reached.

Participants answered questions on their thoughts on and approaches to: transition, risk adjustment, discount rates, reinsurance, KPIs, embedded value, business planning, CSM and loss component, tax, expenses and OCI. A full report will be released in the third quarter of 2023. This article highlights some key findings of the surveys.

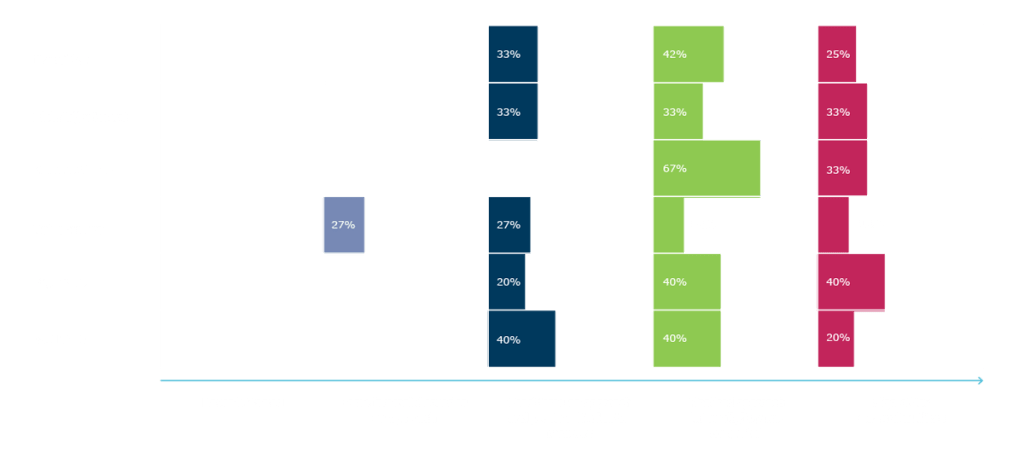

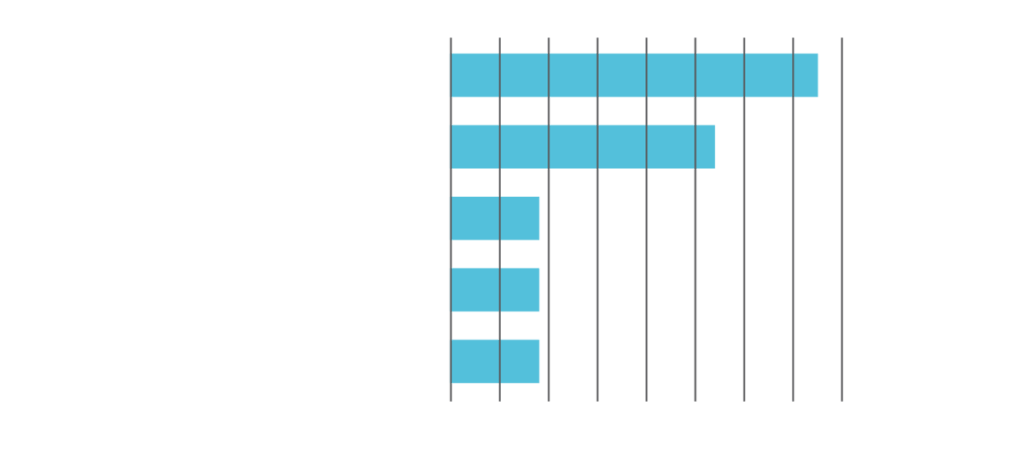

Progress

Respondents were asked to assess their progress on each of the major topics covered by the surveys. The graph below summarises progress across respondents for each topic, with the size of each block representing the proportion of respondents who had reached that milestone.

Figure 1: Participant progress across IFRS 17 topics surveyed

With respect to topics covered by the IFRS 17 Standard, progress seemed to depend on the size of the insurer and the financial reporting period, with larger insurers and those with a 31 December year-end being further progressed than others.

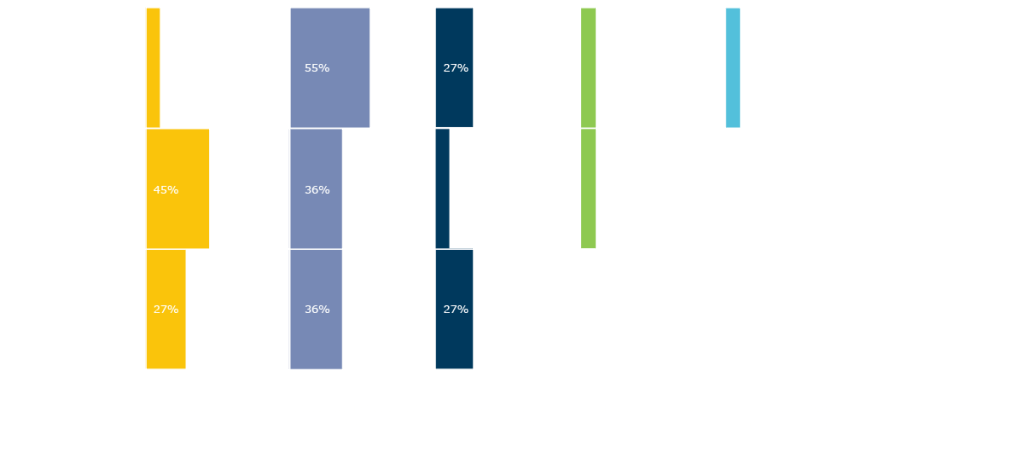

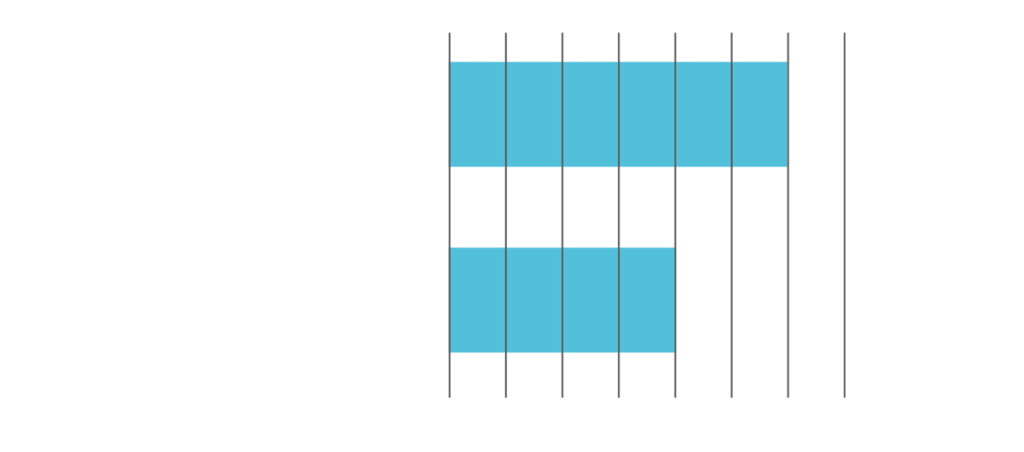

With most of the key methodology and implementation decisions already made, Key Performance Indicators (KPIs), embedded value (EV) and business planning are areas that many insurers have now turned their attention to. The graph below shows progress with respect to KPIs EV and business planning. This graph includes those insurers that do not plan to report EV at all under IFRS 17 (hence the large number who fell into the “haven’t started” category.

Figure 2: Participant progress for KPIs, embedded value and business planning under IFRS 17

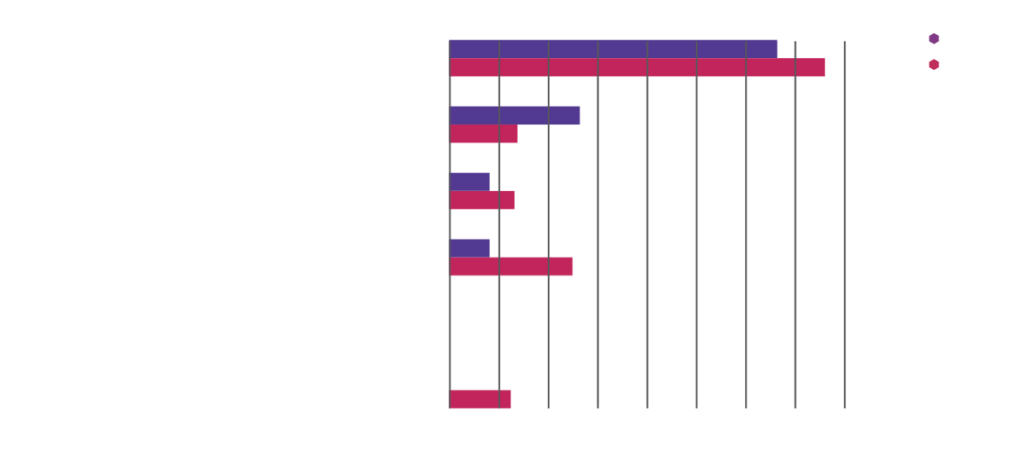

Transition balance sheet

We asked participants whether they expected to see a difference between their IFRS 4 and IFRS 17 balance sheets at transition.

Difference in transition balance sheet

Figure 3: Expected differences in IFRS 4 and IFRS 17 balance sheets

Most respondents expect to see a difference between IFRS 4 and IFRS 17 equity at transition, with half of all respondents expecting IFRS 17 equity to be higher, largely due to having followed a previously more conservative approach to calculating liabilities.

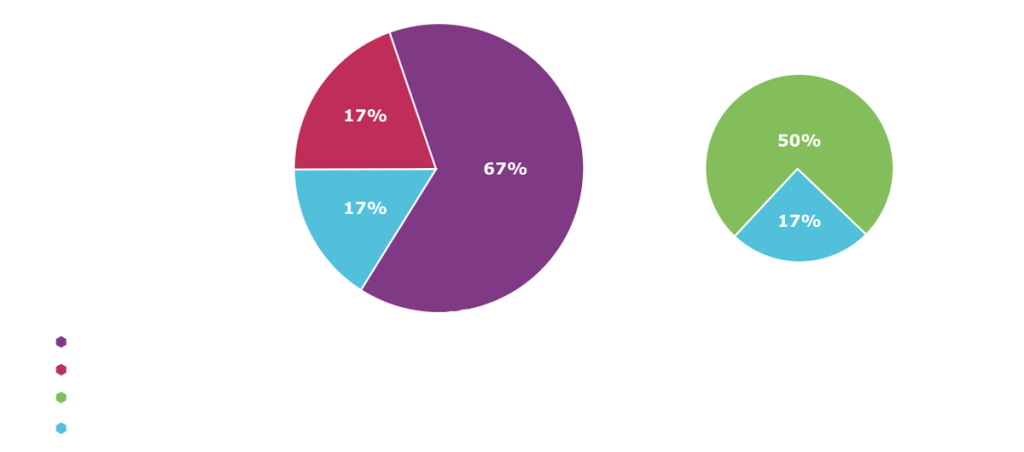

Risk adjustment confidence level

Most respondents are targeting confidence levels of either 75% or 85% for their life business, with the most popular confidence level having decreased from 85% to 75% and 80% over the last year.

Risk Adjustment: targeted confidence level

Figure 4: Targeted risk adjustment confidence level

Locked-in yield curves

Similar to 2022, most respondents in 2023 are using the start of period discount rate for their locked-in yield curves, largely for pragmatism.

None of the respondents indicated that their approach had changed in the last year.

Discount Rates: locked-in yield curve methodology

Figure 5: Approach to calculation of locked-in yield curve

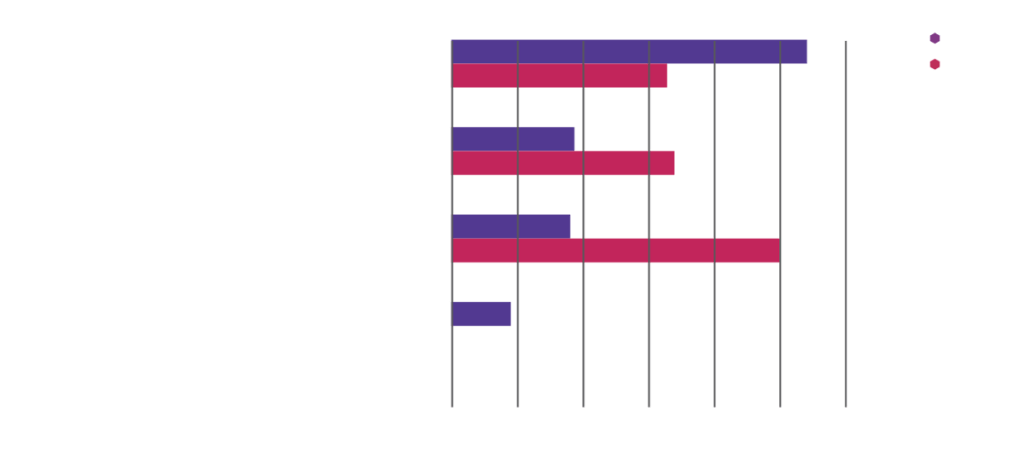

Future new business for reinsurance

In their February 2018 staff paper, the Transition Resource Group for IFRS 17 Insurance Contracts (TRG) said that “…the boundary of a reinsurance contract held could include cash flows from underlying contracts covered by the reinsurance contract that are expected to be issued in the future.”

Insurers therefore need to consider whether and how to measure the cash flows of underlying contracts that have not yet been issued.

In 2023, over half of all respondents are setting their groups and cohorts so that the need to perform this calculation is avoided. Others are projecting future new business as a function of recent new business or based on existing business plans. One respondent does not believe that the projection of future new business is required.

Reinsurance: future new business calculation

Figure 6: Future new business calculation for reinsurance groups

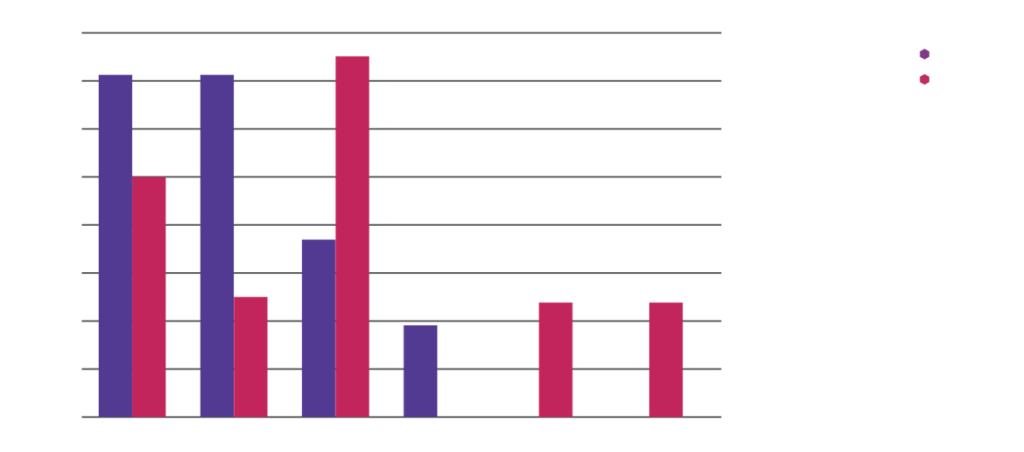

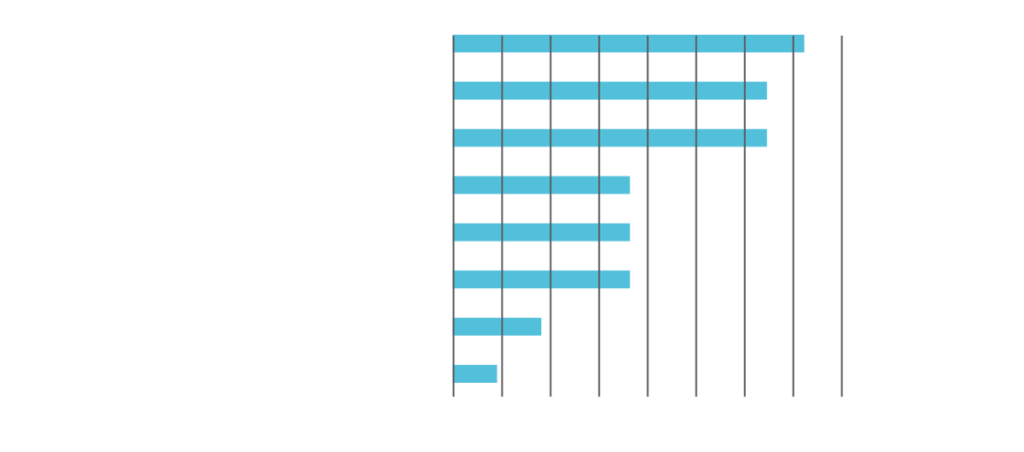

KPIs under IFRS 17

IFRS 17 will change the way insurance accounting works, with new financial statements and methodology for profit emergence. For many insurers, this may mean new KPIs.

Most respondents foresaw Operating Profit, Return on Equity and VNB being their top KPIs under IFRS 17, with some introducing KPIs based on IFRS 17 metrics, such as CSM.

KPI’s measured under IFRS 17

Figure 7: Top KPIs under IFRS 17

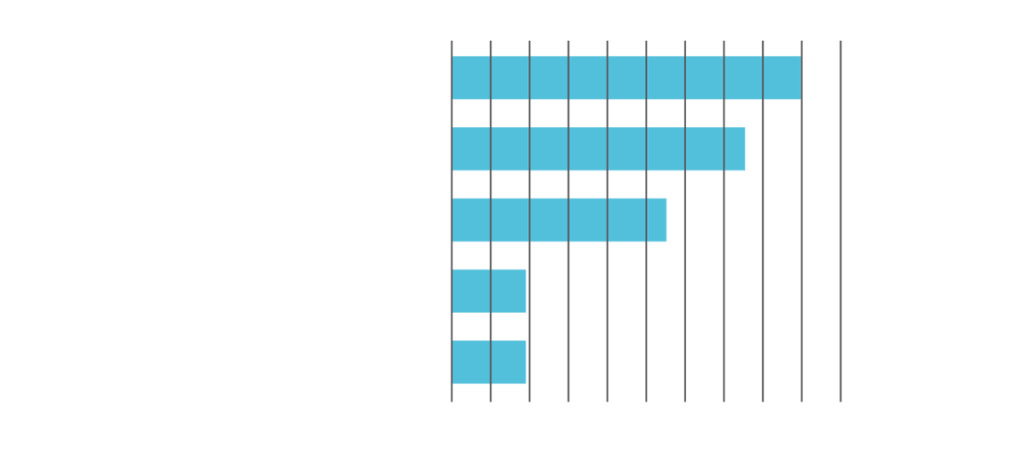

Embedded value under IFRS 17

Most respondents who will produce EV under IFRS 17 have decided to base EV and VNB calculations on the IFRS 17 balance sheet. As can be seen from the graph below, there are some insurers who will not be producing EV at all. This includes reinsurers, part of international groups, that have not produced EV in the past, as well as insurers that will no longer produce EV.

Calculation of EV and VNB under IFRS 17

Figure 8: Calculation of EV and VNB under IFRS 17

Business planning under IFRS 17

Almost all respondents have either performed some kind of business plan or plan to do so within the next year. Challenges around business planning cited by many respondents included: setting budgeting and forecasting methodologies in line with IFRS 17, the manual nature of current processes, and interactions with relevant stakeholders.

Business plan prepared based on IFRS 17

Figure 9: Indication of whether a business plan has been produced based on IFRS 17

Adjustment of coverage units

Expected future coverage units defined in previous reporting periods may need to be revised to account for differences in experience. Insurers need to choose the extent to which they will reflect this revision of coverage units and whether this revision should apply at the start of reporting period or at the end of it.

Most respondents to the survey will update their view of future coverage units to reflect their actual experience, but will not update their coverage units for the current period.

Adjustment of coverage units

Figure 10: Adjustment of coverage units based on experience

These are just a few findings from the series of surveys conducted. Keep an eye on Insight’s social media to download the full report once it becomes available.

This article was featured in the July 2023 edition of the South African Actuary Magazine

View article here

To view the full IFRS 17 Survey Report click here

[1] The 2022 and 2023 participants did not overlap perfectly, so any trends observed between results of the two years are not definitive.

Get an email whenever we publish a new thought piece

Much like rising sea levels, the pressure on South African insurers to address climate‑related risk is steadily climbing. Even if transition risks haven’t yet dented asset values, or physical risks

1.8 min read

At the 2025 ASSA Convention, we polled over 300 actuaries on what they believed was the greatest challenge currently facing their team. While there was a lot of variation in

1.1 min read

Meet our experts

Author

More Insights

Focused Thought Pieces