Mortality Trends in South Africa

15 October 2021

13.7 min read

By Nick van Burick, Nicole Kriek, Zane Heyl, Alwyn Hanekom, Jannus Redelinghuys.

Introduction

Core to the successful operation and management of the life insurance industry is the protection of clients and their dependents in the event of the untimely death and/or disability of loved ones.

In South Africa, the industry has proven that it can protect clients whilst remaining financially and actuarially sound by meeting its obligation despite record high levels of death and illness due to the COVID-19 pandemic.

This blog considers the mortality trends from the mortality claims statistics released by the Association for Savings and Investment South Africa (ASISA), as well as some interesting trends and findings from mortality experience feedback from some of the leading South African life insurers.

ASISA death claim statistics

The below claim statistics were released by ASISA on 31 August 2021 and compares life insurance claims between the period 1 April 2020 to 31 March 2021 (the FY21 year) to those over the same previous 12 months (the FY20 year).

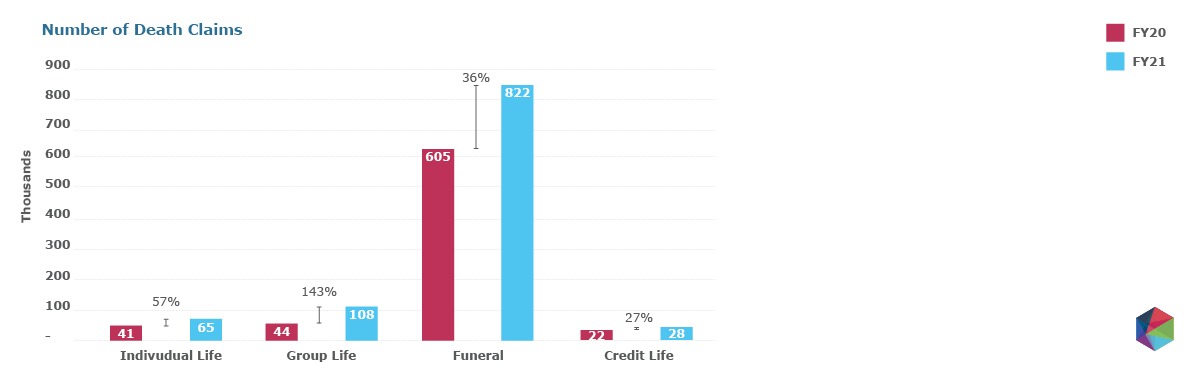

Table 1: Number of death claims, split by line of life insurance business and across comparison years.

The total number of claims increased by 309,733 (43%) with Funeral Life policies representing the largest absolute increase in claim numbers at 216,705 (36%). Group Life business experienced the largest relative increase in claim numbers at 143%.

Based on the reports1 published by the South African Medical Research Council (SAMRC) and the University of Cape Town (UCT) during February 2021, it is estimated that between 85% and 95% of all excess mortality could be attributed to COVID-19.

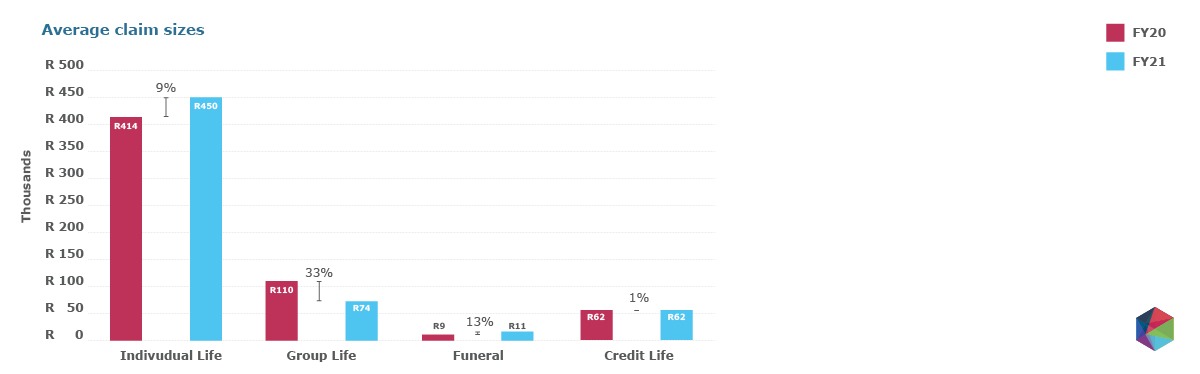

Table 2: Average death claim sizes, split by line of life insurance business and across comparison years.

Individual Life and Funeral business have experienced increases in average claim sizes. These increases were at 9% and 13% respectively.

On the other hand, it is interesting to note that the average claims size of Group Life reduced by 33%. This represents an average, and some insurers did experience increases on their Group Life portfolios.

Insights – average claim size reductions

- Depressed economic conditions with many employers giving little or no salary increases, and even decreases in some cases. About one in five2 employed had a reduction in their pay/salary during the lockdown.

- The expectation is that blue collar schemes had higher levels of exposure to COVID-19 initially due to their working and travelling conditions. As such, for the first wave, the excess mortality will have been weighted towards blue collar schemes. For the second wave, this weighting will have begun shifting towards white collar schemes, but the impact of this wave is potentially dampened due to reporting delays.

- It is possible that a component of Group Life claims occurs as a result of workplace injury so that working from home lessened this issue.

- Increases in the cost of Group Life benefits possibly leading to employers reducing cover amounts such that the overall risk cost remains neutral.

Insights – average claim size increases

Increases to average claim sizes across Individual Life and Funeral books exceeded the inflation rates over that same period. This could in turn be attributed to a higher number of COVID-19-related deaths occurring at older ages where the cover amounts are expected to be higher.

Total claims

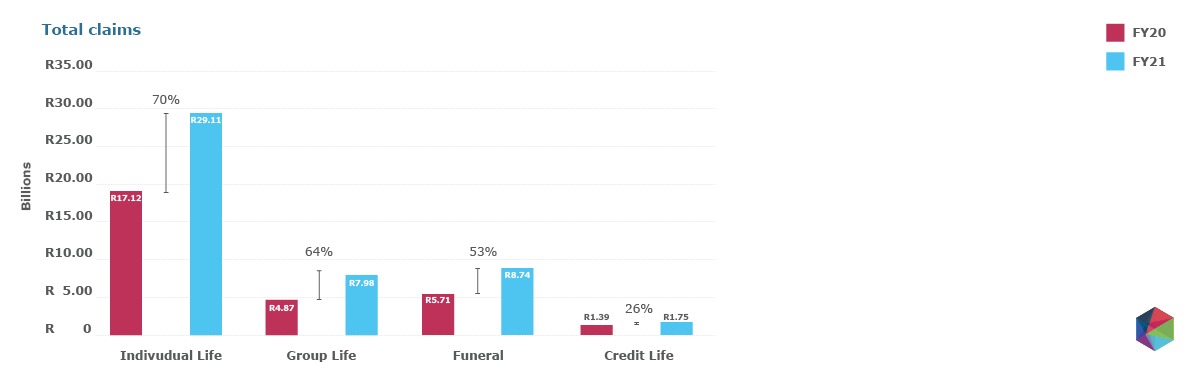

Total claims have increased by R 18.49 billion (64%).

Table 3: Total claims, in billions of ZAR, split by line of life insurance business and across comparison years.

Looking at the insurers

South Africa’s life insurance industry had been hit hard by COVID-19 right from the start of the first wave in March 2020. After the first two waves, even before the third wave began, the country’s largest life insurers reported increases of 50% to 60% in claims against fully underwritten individual life policies in early 2021, with insured lives lost exceeding the expected death rate by four times during the height of the second wave in January 2021.

Due to differences in reporting, and the fact that many large insurers report results on a consolidated level, it is difficult to get the COVID-19 impacts in a comparable format, and even more so for mortality alone. However, we have seen some interesting developments from some insurers.

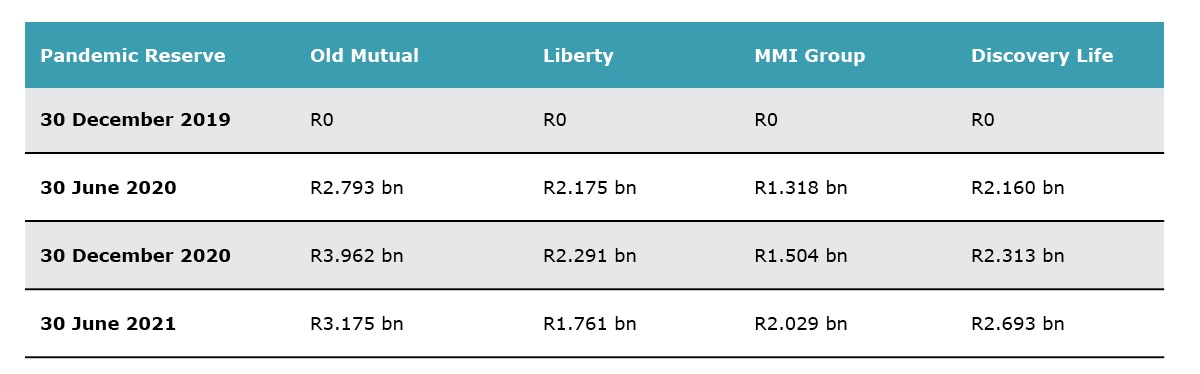

Looking at pandemic reserves, we can develop some insight into initial expectations of the impacts of COVID-19 versus the revised expectation:

Table 4: opening, closing and interim pandemic reserves for big life insurance companies. The data herein was obtained from the relevant financial statements (including interim statements).

Insights – pandemic reserves

It’s interesting to note that all the companies above increased their provisions at the end of 2020 relative to the opening provisions. This was likely as a result of the ramping up of the second wave and revised expectations regarding the runoff of the pandemic.

Discovery Life and MMI Group increased their COVID-19 provisions as at 30 June 2021, whereas the pandemic reserves held by Old Mutual and Liberty reduced from the December 2020 reserves that were established.

Old Mutual has used more than half of its initial R4 billion3 COVID-19 provision to settle COVID-19 related death claims in the first three months of 2021. They also said that only R1.3 billion worth of reserves was left in the kitty, and it was monitoring the situation amid emerging signs of a third wave of infections in SA, which is by far the hardest hit on the African continent.

Old Mutual’s expectation of the total impact of COVID-19 on their claims experience has been revised upwards by R2 billion as of 30 June 2021, to take into account the emerging expectations of the third and fourth waves as well as potential future4 waves. The provisions have been updated to take into account the additional available data to date as well as the anticipated impact of the proposed vaccination rollout plan.

The MMI Group has stated that future mortality experience remains uncertain and is sensitive to the rate at which vaccines are administered.

Insights – an insurer roundtable

Old Mutual

Life insurer Old Mutual’s mortality experience has been worse than anticipated with impact on profits mitigated by a partial release of provisions raised at the end of 2020. Old Mutual has stated that the fallout from the second wave of infections was worse than initially anticipated.

The number of claims Old Mutual received in January 2021 was around double the claims in a normal month.

Insurance premiums are calculated according to complex pricing models which take into account both the current claims environment and the outlook going forward. Until a sufficient number of South Africans have been vaccinated against the coronavirus and the spread of COVID-19 is under control, insurers are likely to err on the side of caution and price their premiums higher.

Sanlam Group Risk

Sanlam Group Risk’s mortality trend5 up to April 2021 has mirrored that of South Africa in terms of shape, except for the second wave where the insured population’s mortality was higher than that of the national trend. According to ASISA, this tendency is consistent across all major insurers and is 400% greater than expected mortality.

During July, August and December 2020, Sanlam Group Risk’s claim amounts were 30%-50% higher than expected, which is slightly lower than the 64% increase in total claim amounts for group business as published by ASISA in the claim statistics released on 31 August 2021.

For January 2021, claim amounts were 300% higher than expected and claim numbers were 250% higher than expected. The increase in average claim size can be attributed to the 45 years and older cohorts which are usually higher income earners with higher cover amounts.

Historically, Sanlam Group Risk used five years of experience data and trends to project their expected experience for the next 12 months to follow. Under current circumstances with COVID-19 Sanlam Group Risk have deemed that the past 12 month’s experience will be a better proxy to project for the next 12 months to follow.

Sanlam CFO Abigail Mukhuba6 has indicated that they would start implementing a number of price and underwriting changes during 2021, however, these changes will be based on a risk-adjusted approach to avoid simply penalizing all unvaccinated individuals. Underwriting and price changes could potentially take into account comorbidities and lifestyle factors to identify high-risk individuals.

MMI Group7

The following are the headline points from MMI Group’s 30 June 2021 financial statements.

- The MMI Group paid out R10.7 billion in gross mortality claims compared to an annual average of R5.6 billion over the three years before the pandemic (a 91% increase).

- The MMI Group experienced mortality claims of R0.702 billion more than expected.

- Total mortality losses for the 2021 financial year ended at R2.831 billion.

During a recent interview, Momentum Metropolitan Holdings CEO, indicated that there is mounting pressure from reinsurers to apply differentiated premium rates for vaccinated and non-vaccinated individuals. The MMI Group has stated that they have seen an improvement in survival rates for vaccinated people relative to non-vaccinated people. The Group’s claims experience indicates that individuals who are not fully vaccinated are 50 times more likely to die from COVID-19 infections than fully vaccinated individuals.

Discovery

Discovery has developed a predictive model to identify the relative risk of hospitalisation for someone diagnosed with COVID-19. The predictive model shows that increased physical activity can mitigate some of the risk that age and chronic conditions add to requiring hospitalisation due to COVID-19. Furthermore, the Index aims to guide people to understand and reduce their risk for possible hospitalisation with recommended lifestyle interventions.

Discovery was the first life insurer to begin using vaccination status as a rating factor8 for writing new business. This, combined with their predictive modelling, may mean that the changes to their mortality rates will remain short-term if the rating factor is not contested.

Liberty9

It’s interesting to note that Liberty reported big spikes in their retrenchment claims. Retrenchment claims peaked between August and October in 2020 on the back of a lag effect from the start of lockdown. During these three months, retrenchment claims peaked at over 60 per month, compared to just over 10 per month during January and February in the same year, showing the effects of the economic contraction at the start of the pandemic.

Also, during the peak of the first wave of the COVID-19 pandemic between June and September 2020, Liberty saw a substantial spike in mortality claims of around 200% above normal levels.

Over half a billion rand was paid out to cover confirmed COVID-related death and health-related claims, of which death was the leading cause. COVID-19 related funeral claims peaked during the first wave with most claims coming from the Eastern Cape, Gauteng and the Free State.

Moving forward

What will be the future trends and levels of mortality remains to be seen. Possibilities include:

- A period of positive mortality experience relative to expected due to the acceleration of deaths for co-morbid lives that would inevitably leave a healthier pool of remaining insured lives.

- Worsening mortality experience due to increases in mortality as dread diseases were left untreated where individuals delayed seeking medical treatment during the peaks of COVID-19.

- Worse than expected mortality due to the yet unknown long-term impacts of COVID-19 (long COVID) on those who have had it.

As new data becomes available over time the life insurance industry can start to develop a better sense of the long-term impact of COVID-19 on South Africa’s medium and long-term mortality trends. COVID -19 has, however, changed the very nature of what we once understood to be normal.

References

1https://www.samrc.ac.za/sites/default/files/files/2021-03-03/CorrelationExcessDeaths.pdf

2Quarerly Labour Force Survey, Quarter 2: 2020, Statistics South Africa

5https://seb-news.sanlam.co.za/wp-content/uploads/2021/07/Research-Insights-Report-2021_MJ.pdf

5https://www.moneyweb.co.za/news/companies-and-deals/covid-19-claims-cost-sanlam-billions/

6https://www.news24.com/fin24/companies/financial-services/r22bn-and-counting-as-sanlam-breaks-death-claim-records-20210909

9https://www.liberty.co.za/media-insights/coping-with-a-spike-in-covid-funeral-claims

For more information and/or to schedule a discussion, contact:

Insight Advisory Solutions

nicovb@insight.co.za

Get an email whenever we publish a new thought piece

The ICHOM 2023 Conference took place in Barcelona this year and was the largest gathering on Value-Based Health Care (VBHC) worldwide. Attended by leading industry experts representing countries from all

2.5 min read

By Insight. "When we die, our bodies become the grass, and the antelope eat the grass. And so we are all connected in the great Circle of Life." – Mufasa

8 min read

Meet our experts

Author

More Insights

Focused Thought Pieces