Rethinking Alternative Reimbursement Models

12 July 2021

9.4 min read

By Poonam Doolabh.

Aside from modelling techniques, there are a few key elements to consider when constructing an ARM contract, as this will affect the answers to the questions above. The list below is by no means exhaustive.

Aside from modelling techniques, there are a few key elements to consider when constructing an ARM contract, as this will affect the answers to the questions above. The list below is by no means exhaustive.

Expected or Target

The expected value or target is the benchmark against which performance is measured. It is important to understand how this is set and what methods are used. This may be a simple projection of current experience with some risk adjustment or based on a more complex machine learning model. Different methods are appropriate for different ARMs.

A tricky conversation between funders and providers is the question of whether a risk premium should be included. Providers usually don’t have reserves or a balance sheet to support extensive risk-taking, so some of the reserve building margin held by funders could be transferred to the provider in the form of a risk premium.

Risk Adjustment

It is important to understand what factors are being used for risk adjustment (such as age, gender, co-morbidities, etc.) and whether more factors could better explain the risk. Insight uses tools such as DRGs, episode groupers and population groupers to perform risk adjustment.

Additionally, parties to the ARM should consider if there is any scope to manipulate risk adjustment factors. There may be a trade-off between the accuracy and reliability of the factors used.

Outliers

The methodology of identifying outliers should be clearly defined and carve-outs should be limited to an acceptable level to avoid an ARM that covers an insufficient number of claims. The reimbursement of the outliers outside of the ARM should also be clearly defined.

Risk-corridors

Risk corridors affect risk-sharing contracts by providing a band around the benchmark within which there is no transfer of funds between the funder and risk-taker. This protects the risk-taker from some level of loss (depending on how wide the risk corridor is). Generally, this is a two-sided arrangement meaning that the funder will expect to share in savings achieved.

Savings

If there are savings expected due to care management interventions, quantifying this with limited experience under new interventions may be challenging. Contracting based on savings expectations may be a delicate undertaking and may sit in another layer of the ARM contract.

Risk-sharing formula

The new contract must specify all the relevant parameters, methods and models in a technical specification. This could be an appendix to the ARM contract. Small changes in these parameters may significantly impact the risk-taker’s risk exposure and having these discussions retrospectively may be problematic.

In summary, successful ARMs require informed decision-making facilitated through the quantification of risks. This helps to better understand the risks, which in turn supports good risk management. Entering into the right ARM design for the right contract structure helps ensure that each party holds appropriate risk. Additionally, regular performance measurement is required as this is key for tracking performance against expected outcomes. If you can’t measure something, you can’t manage it, and if you can’t manage it, you can’t improve it.

¹ Insurance Risk and Its Impact on Provider Shared Risk Payment Models (SOA, 2018)

Expected or Target

The expected value or target is the benchmark against which performance is measured. It is important to understand how this is set and what methods are used. This may be a simple projection of current experience with some risk adjustment or based on a more complex machine learning model. Different methods are appropriate for different ARMs.

A tricky conversation between funders and providers is the question of whether a risk premium should be included. Providers usually don’t have reserves or a balance sheet to support extensive risk-taking, so some of the reserve building margin held by funders could be transferred to the provider in the form of a risk premium.

Risk Adjustment

It is important to understand what factors are being used for risk adjustment (such as age, gender, co-morbidities, etc.) and whether more factors could better explain the risk. Insight uses tools such as DRGs, episode groupers and population groupers to perform risk adjustment.

Additionally, parties to the ARM should consider if there is any scope to manipulate risk adjustment factors. There may be a trade-off between the accuracy and reliability of the factors used.

Outliers

The methodology of identifying outliers should be clearly defined and carve-outs should be limited to an acceptable level to avoid an ARM that covers an insufficient number of claims. The reimbursement of the outliers outside of the ARM should also be clearly defined.

Risk-corridors

Risk corridors affect risk-sharing contracts by providing a band around the benchmark within which there is no transfer of funds between the funder and risk-taker. This protects the risk-taker from some level of loss (depending on how wide the risk corridor is). Generally, this is a two-sided arrangement meaning that the funder will expect to share in savings achieved.

Savings

If there are savings expected due to care management interventions, quantifying this with limited experience under new interventions may be challenging. Contracting based on savings expectations may be a delicate undertaking and may sit in another layer of the ARM contract.

Risk-sharing formula

The new contract must specify all the relevant parameters, methods and models in a technical specification. This could be an appendix to the ARM contract. Small changes in these parameters may significantly impact the risk-taker’s risk exposure and having these discussions retrospectively may be problematic.

In summary, successful ARMs require informed decision-making facilitated through the quantification of risks. This helps to better understand the risks, which in turn supports good risk management. Entering into the right ARM design for the right contract structure helps ensure that each party holds appropriate risk. Additionally, regular performance measurement is required as this is key for tracking performance against expected outcomes. If you can’t measure something, you can’t manage it, and if you can’t manage it, you can’t improve it.

¹ Insurance Risk and Its Impact on Provider Shared Risk Payment Models (SOA, 2018)

For more information and/or to schedule a discussion, contact: Poonam Doolabh poonamd@insight.co.za

We had the pleasure of hosting our second Foresight dialogues event of 2021 with “Reimagine, Rethink and Rebuild” as the theme. Topics included considering the benefits of glucose control monitoring, considering the recovery of elective care, and rethinking alternative reimbursement models (“ARMs”).

See details on our Foresight events here

Rethinking Alternative Reimbursement Models

South Africa’s predominantly fee-for-service environment requires the rebuilding of solutions to align incentives. While many of us are aware of the role ARMs can play in correcting this, little action is implemented in this domain. By aligning financial incentives, providers and funders can prioritise high-quality, cost-effective care to improve patient outcomes instead of negotiating on volumes. One of the pertinent underlying challenges in rebuilding ARMs is contracting. Sometimes, there is a lack of empowerment to have the right discussions because sufficient information for understanding contracting is not available. Sometimes there is a lack of awareness of the risk management options available (mainly due to not understanding the risks taken on). After entering into an ARM, there is sometimes a lack of awareness of the impact that changes in the model parameters can have on risk exposure. This has created mistrust in the industry around ARMs. However, Insight offers strong capabilities of understanding the risks being faced and managing these risks, together with the appropriate tools to quantify the risks, and this collaboration can help to rebuild the use of ARMs in the industry.Risk-transfer vs Risk sharing

To help shed some light on risk in ARMs, we consider the distinction between risk transfer and risk-sharing arrangements. Risk transfer means that the funder transfers risk over to the provider to manage. If we use a DRG based fixed fee ARM as an example, the funder transfers over to the hospital group, the risk of the length of stay (LOS) or level of care (LOC) being higher than expected. The hospital group will be interested in managing LOS and managing patient outcomes to avoid complications to ensure their cost of delivering care does not exceed what is being received under the ARM. If the hospital improves the management of their patients such that LOS or LOC are lower than that priced in the ARM, the hospital enjoys the savings achieved through this improvement. The funder will monitor LOS to ensure patients aren’t being discharged too early, compromising care or resulting in readmissions. Still, they become less concerned with actively managing LOS since this risk has been transferred to the provider. Under a risk-sharing arrangement, using the same example as above, if savings were to occur, some of this would be shared with the funder. Both the funder and the provider would have a vested interest in the LOS being actively managed and monitored, from the hospital’s perspective to manage costs and from the funder’s perspective to actively avoid readmissions and ensure the quality of care. The extent of risk-sharing is a function of the negotiation. In general, risk-sharing contracts are set up such that the provider also shares in losses due to higher-than-expected claims. It is important to remember that risk-sharing contracts can occur in a fee-for-service environment, and many volumes-based discount arrangements started up this way. While these are easier to implement from an administrative perspective (because the reimbursement structure doesn’t need to change), the disadvantage is that incentives are still somewhat misaligned.Additional risks to consider

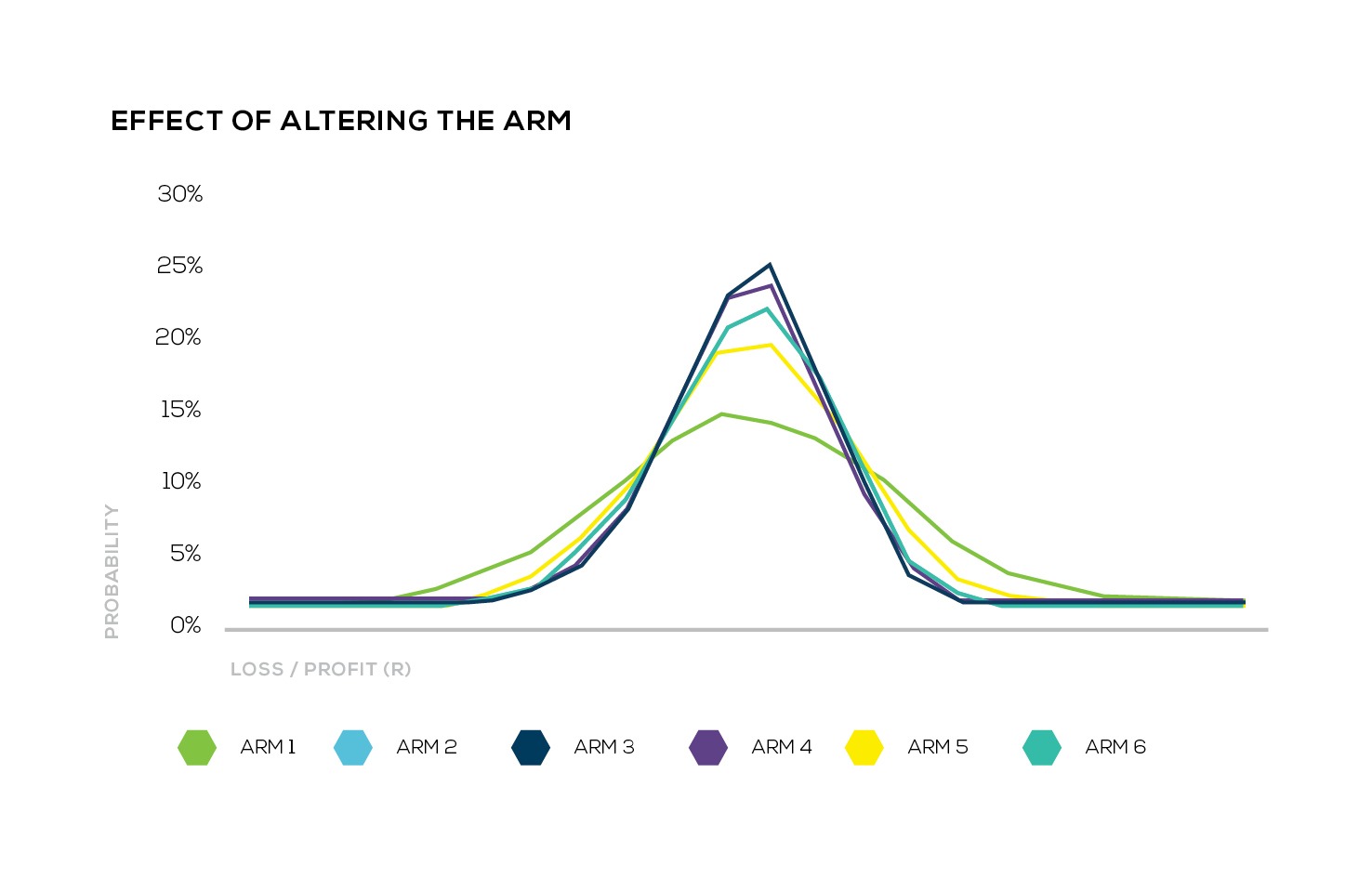

Whilst utilisation, severity and demographic risks are often considered in ARM contracting, two risks often don’t get sufficient consideration when thinking about ARMs. The first risk is pricing risk, the risk that your utilisation levels or any other assumption is wrong or does not pan out as expected under real-world conditions. This is always a risk when designing a new reimbursement model with imperfectly matched data. The estimates derived are ‘best estimates’, which means there is an equal chance that the actual result will be above or below the estimate. The second is stochastic risk, represented by random variation in claims experience. While most of the variation in claims can be explained by certain risk factors such as demographics or case mix, there remains an element of unexplained variation that can only be modelled by a random process. The size of this variation depends in part on the size of the population being managed. ARMs involve taking some stochastic risk that can be directly quantified through techniques such as Monte Carlo simulations. Quantifying risk using stochastic modelling techniques helps to address the following questions¹:- What is the best estimate of my future performance?

- What is the range of possible outcomes?

- What is the risk of loss? What is the maximum amount at risk?

- What is the likelihood of savings?

- How can altering the ARM impact the range of results?

Aside from modelling techniques, there are a few key elements to consider when constructing an ARM contract, as this will affect the answers to the questions above. The list below is by no means exhaustive.

Aside from modelling techniques, there are a few key elements to consider when constructing an ARM contract, as this will affect the answers to the questions above. The list below is by no means exhaustive.

Expected or Target

The expected value or target is the benchmark against which performance is measured. It is important to understand how this is set and what methods are used. This may be a simple projection of current experience with some risk adjustment or based on a more complex machine learning model. Different methods are appropriate for different ARMs.

A tricky conversation between funders and providers is the question of whether a risk premium should be included. Providers usually don’t have reserves or a balance sheet to support extensive risk-taking, so some of the reserve building margin held by funders could be transferred to the provider in the form of a risk premium.

Expected or Target

The expected value or target is the benchmark against which performance is measured. It is important to understand how this is set and what methods are used. This may be a simple projection of current experience with some risk adjustment or based on a more complex machine learning model. Different methods are appropriate for different ARMs.

A tricky conversation between funders and providers is the question of whether a risk premium should be included. Providers usually don’t have reserves or a balance sheet to support extensive risk-taking, so some of the reserve building margin held by funders could be transferred to the provider in the form of a risk premium.

Risk Adjustment

It is important to understand what factors are being used for risk adjustment (such as age, gender, co-morbidities, etc.) and whether more factors could better explain the risk. Insight uses tools such as DRGs, episode groupers and population groupers to perform risk adjustment.

Additionally, parties to the ARM should consider if there is any scope to manipulate risk adjustment factors. There may be a trade-off between the accuracy and reliability of the factors used.

Risk Adjustment

It is important to understand what factors are being used for risk adjustment (such as age, gender, co-morbidities, etc.) and whether more factors could better explain the risk. Insight uses tools such as DRGs, episode groupers and population groupers to perform risk adjustment.

Additionally, parties to the ARM should consider if there is any scope to manipulate risk adjustment factors. There may be a trade-off between the accuracy and reliability of the factors used.

Risk-corridors

Risk corridors affect risk-sharing contracts by providing a band around the benchmark within which there is no transfer of funds between the funder and risk-taker. This protects the risk-taker from some level of loss (depending on how wide the risk corridor is). Generally, this is a two-sided arrangement meaning that the funder will expect to share in savings achieved.

Risk-corridors

Risk corridors affect risk-sharing contracts by providing a band around the benchmark within which there is no transfer of funds between the funder and risk-taker. This protects the risk-taker from some level of loss (depending on how wide the risk corridor is). Generally, this is a two-sided arrangement meaning that the funder will expect to share in savings achieved.

Savings

If there are savings expected due to care management interventions, quantifying this with limited experience under new interventions may be challenging. Contracting based on savings expectations may be a delicate undertaking and may sit in another layer of the ARM contract.

Savings

If there are savings expected due to care management interventions, quantifying this with limited experience under new interventions may be challenging. Contracting based on savings expectations may be a delicate undertaking and may sit in another layer of the ARM contract.

Risk-sharing formula

The new contract must specify all the relevant parameters, methods and models in a technical specification. This could be an appendix to the ARM contract. Small changes in these parameters may significantly impact the risk-taker’s risk exposure and having these discussions retrospectively may be problematic.

In summary, successful ARMs require informed decision-making facilitated through the quantification of risks. This helps to better understand the risks, which in turn supports good risk management. Entering into the right ARM design for the right contract structure helps ensure that each party holds appropriate risk. Additionally, regular performance measurement is required as this is key for tracking performance against expected outcomes. If you can’t measure something, you can’t manage it, and if you can’t manage it, you can’t improve it.

¹ Insurance Risk and Its Impact on Provider Shared Risk Payment Models (SOA, 2018)

Risk-sharing formula

The new contract must specify all the relevant parameters, methods and models in a technical specification. This could be an appendix to the ARM contract. Small changes in these parameters may significantly impact the risk-taker’s risk exposure and having these discussions retrospectively may be problematic.

In summary, successful ARMs require informed decision-making facilitated through the quantification of risks. This helps to better understand the risks, which in turn supports good risk management. Entering into the right ARM design for the right contract structure helps ensure that each party holds appropriate risk. Additionally, regular performance measurement is required as this is key for tracking performance against expected outcomes. If you can’t measure something, you can’t manage it, and if you can’t manage it, you can’t improve it.

¹ Insurance Risk and Its Impact on Provider Shared Risk Payment Models (SOA, 2018)

For more information and/or to schedule a discussion, contact: Poonam Doolabh poonamd@insight.co.za

Get an email whenever we publish a new thought piece

In 2023, Insight Life Solutions conducted a series of surveys to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the progress made

3.2 min read

Insight Life Solutions conducted a series of five surveys in Q3 2022 to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the

3.5 min read

Meet our experts

Author

More Insights

Focused Thought Pieces