The Signal Model: Throwing Light into Dark Corners

11 July 2016

15.3 min read

Murky territory

Have you ever tried to compare the value-for-money that you get from two different medical scheme options? Whether you’re a consumer trying to choose an option, a broker advising clients or a technical marketing actuary, you will know that it is impossible to come to an objective conclusion by simply studying the benefit brochures. Simply tallying which benefit option offers richer benefits is insufficient, particularly since you need to make a comparison on multiple benefits. The question that needs to be asked is “what is the value of those additional benefits and how does it compare to the cost of monthly contributions?”

Trying to determine how much a consumer can be expected to “get out” based on a comparison of benefits is difficult enough that most people don’t even try. Instead most consumers base their option choices on affordability (i.e. how much can they afford or are they willing to pay for a specific set of benefits), personal health circumstances (“I have this condition or need that operation and this option covers it”) or advice (which is not necessarily well informed).

How can a more expensive option offer poorer benefits?

People commonly assess value based on price. In a competitive market it is valid to assume that expensive products are “better” than more affordable products, since a rational market would not purchase expensive low quality versions when there are better alternatives available. Unfortunately, the market for medical scheme benefits is not like this.

Aspects of the current regulatory environment, specifically community rating in the absence of risk equalisation, means that the contribution rates of medical scheme options depend greatly on the risk profile of the beneficiaries who belong to that option. Healthcare for older and sicker people costs more on average than healthcare for the young and healthy and these costs need to be funded from contribution income.

When you buy comprehensive cover, part of the additional cost is because the benefits are richer, whilst the rest is because sicker people tend to buy more comprehensive cover than healthy people. The latter has a much greater impact on the cost of providing the benefits than the benefit design.

In this environment it is therefore possible to construct a scenario where a scheme with a poor risk profile would only be able to offer limited benefits at comprehensive option prices. Conversely we can picture a scenario where comprehensive benefits can be offered at relatively low prices, simply due to healthier risk profile. The contribution level is therefore not a good proxy for benefit richness and is far more accurate as an indicator of the options’ demographic profile.

Is an objective comparison even possible?

A recent survey[1] of medical scheme benefit options contained the following sentence (emphasis added):

“Whilst we acknowledge again this year that the direct comparison of many of the schemes in the different categories is almost impossible, we have once again grouped the plans to ensure the closest “apples for apples” type comparisons amongst competitors in each category.”

We must respectfully disagree. It may seem like a daunting task to make such direct comparisons but that does not make it impossible.

As actuaries we like to believe that most things can be measured, quantified and exhaustively analysed. We also recognise that the results of a scheme-value comparison are only meaningful if sufficient rigour and expertise are applied to the task. Decoding the complexity of medical scheme benefit design is just the sort of challenge we love. Being actuaries, we approached the problem by building a model.

The Signal Model[2] is a tool we created to compare the benefit richness of different medical scheme options in an objective manner. The model allows us to compare options across medical schemes.

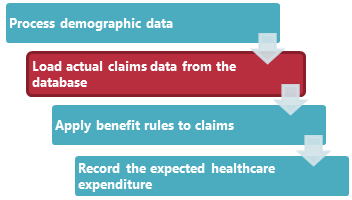

The basic premise underlying the Signal model is quite simple: simulate the medical scheme world in computer code. This entails the capturing of the information in benefit brochures as rules understood by software. The software will then apply these rules to a given set of claims. The claims data will be the same for every option we simulate. We use this standardised set of claims to remove factors such as demographic differences from the analysis and to compare like with like. Using real world data is the best way to incorporate the correlation between claims from one month to the next into our calculations.

Easy, right? As it turns out: no, not really. The basic idea may be simple but the devil is in the detail.

Data, data, data

The first step to constructing our Signal model is to find a standard set of real world claims that is representative of all medical scheme beneficiaries. For example, if we only used the claims of twenty-something Super-15 rugby players then we would be able to compare schemes very well on the basis of how well they cover the claims arising from sport injuries (and accidents involving fast cars) but would miss out aspects such as chronic conditions associated with age, maternity benefits, diseases caused by sedentary lifestyles and so forth.

We therefore need to include a variety of beneficiaries with an assortment of claiming patterns. This data set is referred to as the “standard population”. Only beneficiaries who were on a scheme for the entire year (from January to December) are included in the sample population, with the exception of newborns who may be included for part of the year.

For this standard population, we not only require the claims data but also data relating to the underlying members and their dependants, since some of the benefit limits depend on family structure. Certain limit amounts are based on the size or composition of the covered family, or may even be expressed as a proportion of contributions. We also calculate contributions (allowing for income-rated contributions) since price is the other side of the value-for-money equation.

The standard population is divided into cells based on the following factors:

- Current option type

- Age

- Gender

- Chronic status

- Family size and

- Claims level[3]

We also need to ensure that we include and model all the benefit categories that are common across medical schemes. Each claim is allocated to one of 36 claim types. The model includes episodes of care pertaining to procedure-specific claim types (for example, gastroscopies) in order to allow us to simulate the most common co-payments that schemes levy. Doing so also allows for exclusions. Such exclusions may have a significant impact on the benefit richness calculation. For example, some options will only pay for joint replacements that are part of the Prescribed Minimum Benefit (PMB) package whereas others will cover non-PMB replacements as well, subject to a limit. For older members this can become quite important.

As we also need to realistically allow for the impact of PMBs on benefit richness, the claims data includes a PMB indicator. PMB claims are always paid from risk benefits without limit or co-payment.

Modelling benefits and running the simulation

In order to model benefits, we are essentially replicating the capability of an administration system that would apply these rules. Describing a set of benefits therefore involves the definition of logical rules, including limits and co-payments.

For each benefit category we then have to specify the benefit rules. This involves choosing a benefit processing algorithm to apply to a specific benefit and then specifying a set of parameters. Most of these parameters are used to “wire” benefit limits to the rule algorithm in the correct order of processing. For example the rule may be “always pay claims in this benefit category” or “pay this benefit from limit X, subject to overall limit Y.”

Each individual claim is loaded into the model chronologically and the software then applies the rules, as well as the limits that apply to the patient and his/her family, to determine how much the scheme would pay out, either from risk benefits or personal medical savings accounts. The available limits and balances are updated to reflect the result of the transaction.

With a large volume of claims (7.2 million claim lines) to process, for each option being compared, as well as the number of limits that must be stored, running the simulation becomes computationally intensive. The Signal model software has been optimised for this task but still requires a powerful computer to run.

No trivial task

According to the CMS 2015 annual report there were 25 open medical schemes with 138 registered benefit options as at 31 March 2015. Note that this excludes restricted schemes that may be included in an analysis (depending on the needs of the client). This represents a lot of work, particularly since capturing and simulating these benefits is not a trivial task.

The benefit designs must be captured in a standard format that strikes the correct balance between detail and simplicity. If we do this at too high a level, then we will not be able to show the differences between options based on important benefit distinctions. Too much detail and the modelling and data capture becomes significantly more onerous, with no payback in terms of greater accuracy in the results. Capturing benefit rules takes time, requires judgement and problem-solving abilities, and cannot really be automated or simplified. The task is made all the more difficult because of the variety of benefit structures and the lack of industry standardisation.

The array of benefit structures is astounding. New generation options have medical savings accounts. There may also be above threshold benefits that apply once your medical savings have been exhausted (and you have burned through any self-payment gap). With traditional benefits it does not get any simpler. Is the benefit limited to an amount available for each beneficiary or a limit that applies to the whole family? It may even be a combination of beneficiary and family level limits. What about cases such as a combined limit for different benefits. Is a R2,000 combined limit for radiology and pathology the same as two separate R1,000 limits for each of these categories? Certain benefits are limited based on number rather than amount (e.g. 12 GP visits per family per annum, or one pair of spectacles every two years). In some cases, benefit structures may be very different from the rest of the industry and don’t fit neatly into the typical approach followed by most other schemes, in which case some customisation may be necessary.

The lack of industry standardisation extends from the way brochures are laid out to variations in terminology. All of which brings us back to the starting premise: “Have you ever tried to compare the value-for-money that you get from two different medical scheme options?”

We have gone through a number of iterative designs to come up with a model that successfully allows for all of these possibilities while remaining maintainable and flexible enough to meet future requirements, as they arise.

One size does not fit all

Attempting to construct a tool that tries to compare all medical scheme options on a single continuous scale in a one-size-fits-all approach cannot provide all of the answers. For one thing, members will assess value differently depending on their individual risk preferences and health needs. For example, we can understand that a low-claiming single man in his twenties will find less value in a comprehensive option than a 55-year old with a chronic condition and a large family. In another case we may see that an option offers good value, so long as you don’t have a family comprising more than four people, because of the way day-to-day limits are expressed. This is where the power of the model comes in: we can drill down into the model results based on any of the population factors (such as age) that are included in the model and use it to reach reasonable conclusions based on context.

The Signal model is currently focussed on comparing options based on explicitly defined benefits and contributions. There are other facets which are more difficult to capture and codify (for example, protocols, authorisation rules, provider networks and the quality of care purchased) which we will be working to incorporate in the future.

Simple solutions for complex problems

“For every complex problem, there is an answer that is clear, simple, and wrong” – H L Mencken, 1917

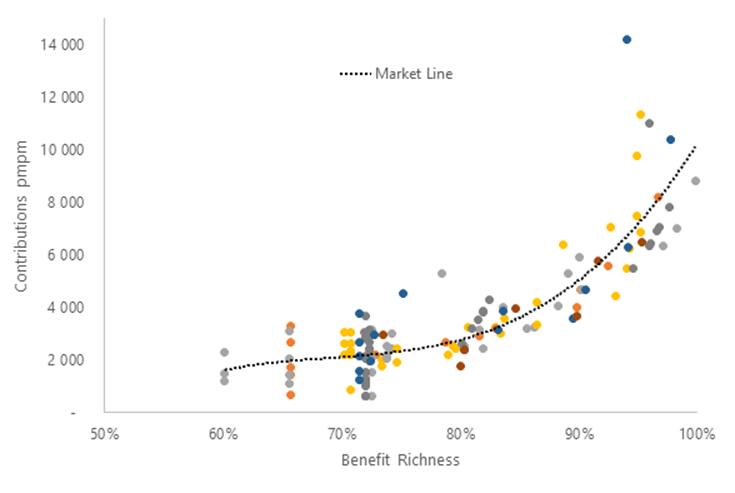

Medical scheme benefit design is multi-faceted and highly variable. Consequently, comparing the value offered by medical scheme benefit options is a complex task. A simple solution will therefore, almost inevitably, be wrong. This does not, however, mean that it is impossible to do. The results from the Signal model indicate that doing the work is worthwhile. The graph below illustrates the relationship between price and benefit richness for seven large open schemes. Each dot represents an income-banded contribution level for an option. It is clear that the relationship between the two is by no means straightforward. This emphasises the risk associated with overly simplified (and probably incorrect) comparisons.

A meaningful comparison of benefit option value requires clever software design, skilled data capturing, meaningful data and significant computing power. It also requires constant revision and review to ensure that the results are meaningful and up to date. Insight has been working on the problem for some time now and we are confident that the approach contemplated in the Signal Model offers a powerful and scientifically accurate manner in which value for money can be assessed.

[1] GTC (June 2016). The GTC Medical Aid Survey: Benefit and cost comparison – 2016. Retrieved from http://www.gtc.co.za/wp-content/uploads/2016/06/GTC-MAS-2016-A4-DOWNLOAD-SMALL.pdf

[2] Why is it called the Signal Model? Maybe because we love the book “The Signal and the Noise” by Nate Silver

[3] Claims level divides the families into High, Medium and Low claiming groups (compared to their peers with the same characteristics).

Get an email whenever we publish a new thought piece

The ICHOM 2023 Conference took place in Barcelona this year and was the largest gathering on Value-Based Health Care (VBHC) worldwide. Attended by leading industry experts representing countries from all

2.5 min read

By Insight. "When we die, our bodies become the grass, and the antelope eat the grass. And so we are all connected in the great Circle of Life." – Mufasa

8 min read

Meet our experts

Author

More Insights

Focused Thought Pieces