We told you so

Medical schemes operate in an incomplete regulatory environment. The package of reforms of which began with Act 131 was intended to improve social protection.

16 September 2024

8.9 min read

Image by hornbillsstudio on Freepik

Part of the job of an actuary is to form a view on the future taking into account the past and expected future developments. This allows us to help stakeholders price insurance contracts, hold appropriate levels of capital and manage risk.

The healthcare financing reform pathway South Africa has followed has been complex and political. The Medical Schemes Act 131 of 1998 implemented from 2000 onward was part of a larger set of planned reforms intended to improve healthcare financing coverage. It is common cause that from 2007 the country’s health reform trajectory changed direction towards a single payer model, the National Health Insurance. This article is not about the NHI, but rather about medical schemes.

A significant part of the criticism levied at medical schemes are their high cost, and persistently higher than inflation rates of contribution increases, typically CPI plus 3% or 4%.

Medical schemes operate in an incomplete regulatory environment. The package of reforms of which began with Act 131 was intended to improve social protection through

- open enrolment (applicants cannot be declined such as happens in most other forms of insurance),

- prescribed minimum benefits (to ensure product design does no discriminate against the sick and elderly) and

- community rating (so that members pay the same for the same cover regardless of age and state of health).

While these three social protection reforms each establish admirable and necessary goals, each of them also introduces costs and risks to the system. This was understood by policymakers from the outset, and the intended reforms therefore included further sustainability reforms that would be required to mitigate the potential negative impacts of the social protection reforms.

Part of these sustainability reforms were to:

- introduce mandatory membership of medical schemes for citizens earning above some level of income (to prevent anti-selection into and out of the risk pool environment) and

- a risk equalisation fund (to prevent selection and cherry picking between medical schemes).

There was sincere concern in the actuarial profession that implementing the social protection elements of the reforms without the sustainability reforms would lead to escalating costs due to anti-selection, the so-called “actuarial death spiral”. Presentations were made in parliament in 1997 warning of the risk of a death spiral which arises when anti-selection drives medical scheme claims costs and resultant contributions higher than need be. This, in turn, makes medical schemes less attractive in terms of value for money for young and healthy individuals who opt out, which in turn drives costs up further and so on. Medical schemes are largely powerless to mitigate this risk due to the limited ability to underwrite through waiting periods. Late joiner penalties have also proven ineffective at reducing the anti-selection risk.

Significant work was done on a risk equalisation fund for the sector in the early between 2004 and 2006, resulting in the publication of a draft amendment bill that would have enabled the REF in 2006 and 2007, but the REF was not implemented. No meaningful work was done towards mandatory membership. The shift in policy to move directly to a single funder NHI at the 2007 Polokwane elective conference ground all meaningful medical scheme regulatory reform to a halt, including the implementation of reforms intended to make schemes more sustainable.

Since 2000 then, the medical scheme environment has had the conditions actuaries had feared with anti-selection driving real cost escalation. It is cold comfort to now say – we told you so. Medical schemes and their administration and managed care agents have worked hard over the past two decades to minimise the cost escalations, but contributions still increase steadily above inflation.

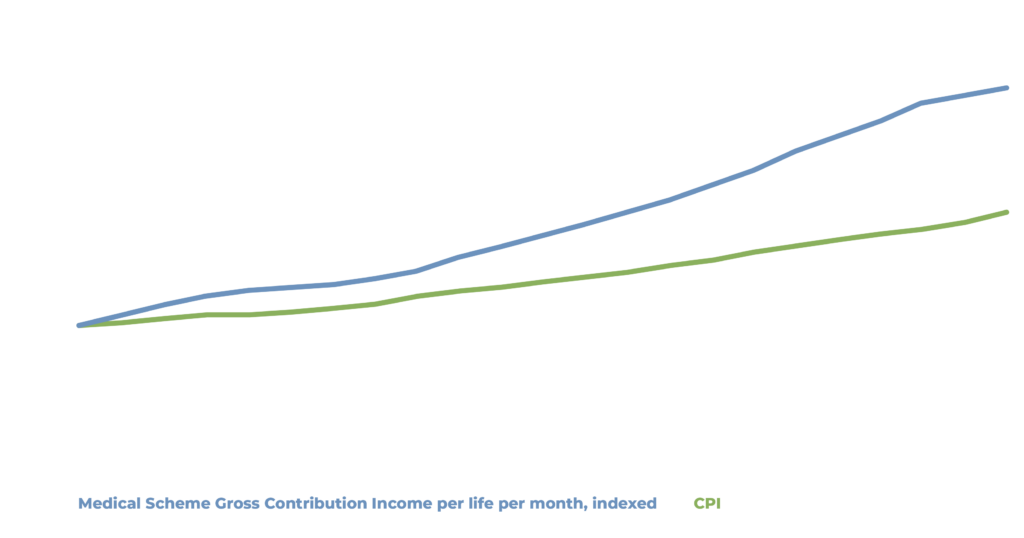

Medical scheme gross contribution income over time is muted by several factors including option buydown, and diminishing benefits (for example lowering medical savings account contributions and benefits). Over the 22 year period medical scheme Gross Contribution Income (GCI) per life per month increased 8.2% per annum while CPI increase 5.5%. Comparing the long-term difference, medical schemes would be 43% cheaper today than they are currently if contributions had escalated at CPI.

Part of the reason for these increases has been the continuing deterioration of medical scheme risk, both because of anti-selective joining and leaving and also because of product downgrades over time – both of which could have been avoided if government followed through on its original intentions to supplement social protection reforms with sustainability reforms.

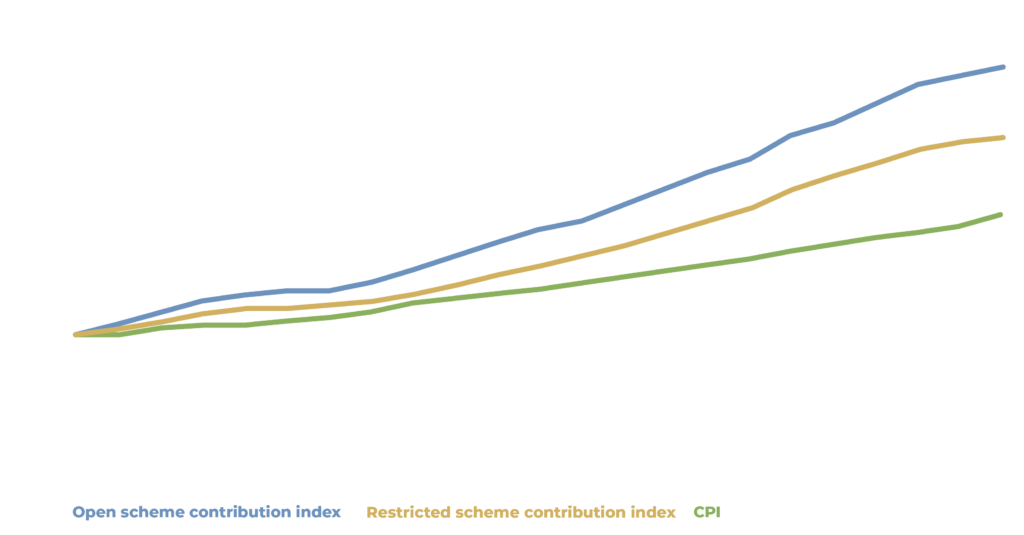

We can also demonstrate this dynamic with historical data by comparing contribution increases of open medical schemes and restricted medical schemes. Restricted medical schemes are confined to an employer, or industry, and suffer far less anti-selection than open medical schemes who must accept anyone who applies.

While still above inflation, restricted medical scheme contribution increases have been significantly less than open medical schemes, despite operating in the same environment. The only material difference on cost driving pressure between open and restricted medical schemes is the presence of more severe anti-selection. Restricted schemes still have some elements of anti-selection as company benefits policies may allow employees to opt out of they are already covered on a spouses medical aid, and there is no mandate requiring all members of the employees family to be on the scheme. As costs have increased this has caused families to be selective about which members to include on cover (evidenced by the long term trend of smaller medical scheme membership family size). Restricted medical scheme contribution inflation over the 22 year period was 7.4% while open medical scheme contribution inflation was 8.7%. This puts a floor estimate on anti-selection at 1.3% per annum. Accumulated over the 22 year period, we can infer that open medical schemes could be 23% cheaper than current prices, if they were exposed to the same level of anti-selection as restricted schemes.

Restricted scheme inflation is still notably higher than CPI (1.9% per annum). Some restricted schemes operate in a competitive environment and allow choice of cover. In these schemes, some of which are sizeable, restricted schemes compete with open schemes for members and are exposed to anti-selection risk. One risk mitigation for anti-selection is the application of underwriting (which is far more limited in the medical scheme environment than other insurance markets) and application of late joiner penalties (which are intended to disincentivise joining medical schemes only when old and sick). Open medical schemes are usually diligent when it comes to underwriting and application of LJPs as these are their only real defences against anti-selection. Restricted schemes that operate in competitive environments also make use of underwriting to some degree. Using data for such schemes during period when they did and did not apply such underwriting we can test the level of anti-selection in the restricted scheme environment.

Based on our analysis we can put the effect of anti-selection in restricted schemes at around 1% per annum. This means that without anti-selection, restricted schemes would have increased less than 1% above CPI over the past 22 years. This means even restricted medical schemes could have been 20% lower than current prices without the effect of anti-selection.

While the term “death spiral” seemed dramatic at the time of warning, contribution increases 3.2% above inflation over such long period of time are significant enough that we can declare the warning sound. However, this hindsight is not helpful as there appear to be no plans to complete the medical scheme regulatory environment with the sustainability reforms discussed above, due to the focus of all regulatory reform being on NHI. This is despite the thoroughly researched findings and recommendations of the Health Market Inquiry (September 2019) which suggested similar reforms to those that were supposed to be introduced in the early 2000’s.

So, when criticisms are levied at the high level of medical scheme contributions, or the high rate of increases in contributions, or diminishing benefits over time, we must remember a large driver of real contribution inflation is because well planned and critical regulatory reforms for the sector were never implemented, leaving schemes at the mercy of anti-selection to the tune 40% cumulatively over the last 22 years.

Get an email whenever we publish a new thought piece

From time to time I get asked to talk about the Social Determinants of Health (SDH). Broadly speaking the SDH are drivers of health other than healthcare and healthcare financing

2.5 min read

Meet our experts

Author

More Insights

Focused Thought Pieces