What goes down must come back up

“How can we give reserves back to members?” On the surface, this seems like such a simple question. But as it turns out, giving reserves back to members is surprisingly hard to do.

27 September 2024

5.9 min read

Image by stock.com

During the Covid-19 pandemic, medical schemes saw reduced claims from their members. While medical schemes paid significant amounts towards Covid-related PCR tests, medication, consultations and hospitalisation, this was more than offset by reduced utilisation of other medical scheme benefits.

As a result, medical schemes made large surpluses in 2020 and 2021 and built up high reserves during this time.

By law, a medical scheme is a not-for-profit entity – very similar to a Trust fund. The funds in a scheme belong entirely to the members and can only be used towards the benefit of members.

As reserves started building up during Covid-19, medical scheme Trustees started asking themselves how high reserves can best be applied to assist and support members – bearing in mind the financial hardship suffered by many South Africans during lockdowns.

“How can we give reserves back to members?” On the surface, this seems like such a simple question.

But as it turns out, giving reserves back to members is surprisingly hard to do.

How to perform responsible “reserve shedding”

Schemes considered many mechanisms to give reserves back to members. Some schemes even explored the possibility of paying a lump sum of cash to each member, or injecting a lump amount into members’ medical savings accounts. Unfortunately, section 26(5) of the Medical Schemes Act impose quite severe restrictions to a medical scheme’s ability to make special payments to members, stating that “No payment in whatever form shall be made by a medical scheme directly or indirectly to any person as a dividend, rebate or bonus of any kind whatsoever.”

For most medical schemes, therefore, it would appear that the only way to give reserves back to members is to budget for a loss.

This can be done by:

- Temporarily making contributions lower than they would have been; and/or

- Temporarily making benefits higher than they would have been.

By doing one or both of these, a medical scheme deliberately starts making losses. Reserves are used to pay claims or expenditure that are higher than the contributions received. Indeed, this is what many medical schemes started doing from 2021 onwards.

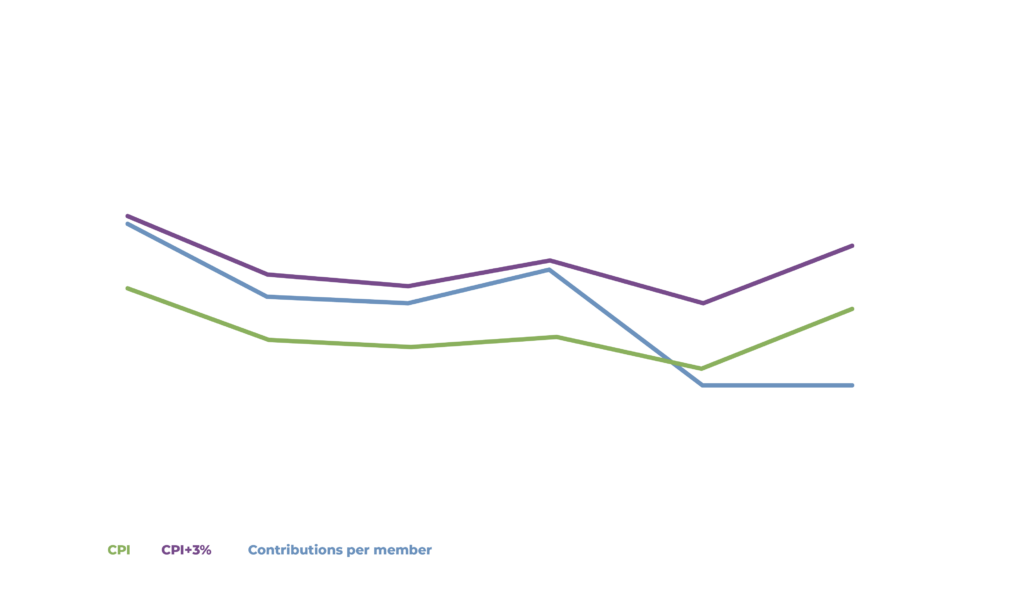

Medical inflation is widely held to be in the region of CPI+3% or CPI+4%. The reasons for this number being higher than CPI is a topic that requires a blog of its own, but suffice to say here that the ageing population, anti-selective joining and withdrawing from schemes, and new medical technologies all contribute to the fact that medical inflation is higher than CPI. However, in 2021 and 2022, many medical schemes opted to increase their contributions by less than CPI. We saw some schemes increasing contributions by as low as 2% or 4%, and a few schemes even marginally reduced their contributions.

This graph presents averages, and in reality there was a whole range of activity around these averages. Some medical schemes increased their contributions with figures closer to CPI. Some medical schemes opted to delay contribution increases towards the middle of the year, but still increasing the delayed increase in line with inflation.

The result of these lower contribution increases during Covid was that schemes started making losses. Making losses sounds wrong, but these losses were deliberate. Within the restrictive confines of what the Act allows Trustees to do, this was, generally speaking, the only way in which Trustees can ensure that reserves that built up during the pandemic will slowly flow back into the hands of members.

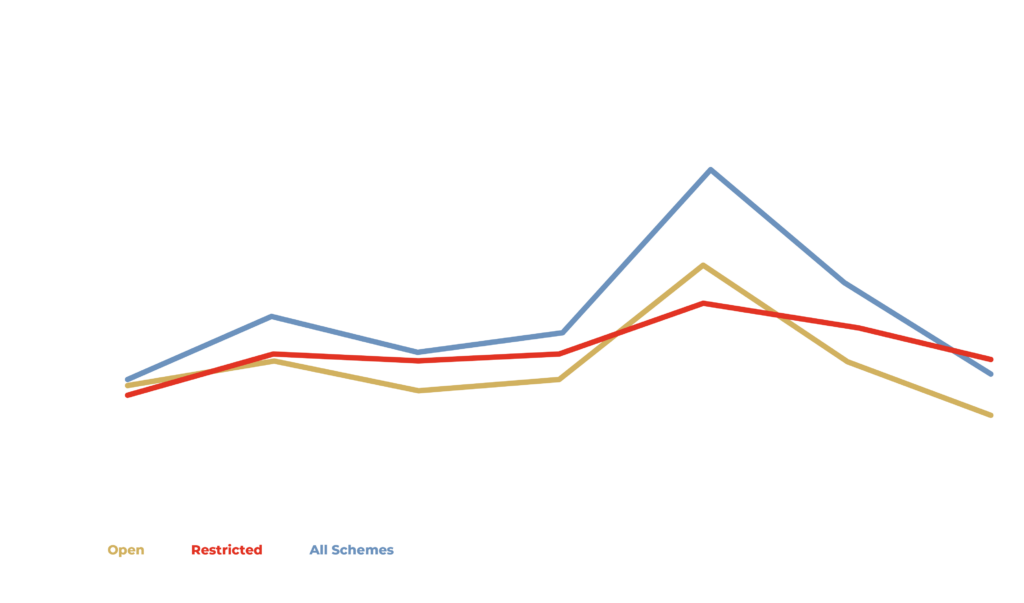

After high surpluses in 2020, the loss-making strategy showed results coming back to normality, with open schemes posting losses in 2022. At the time of writing this blog, the 2023 results are not yet publicly available – but most open schemes continued making significant losses in 2023. At the time of writing this blog, many schemes’ reserves have now returned to “conventional” pre-Covid levels.

Members have enjoyed lower contributions over the past few years. Unfortunately, it seems that many schemes will now need to bring pricing back to sustainable levels. This will mean higher contribution increases into 2025.

The problem with making losses, of course, is that you can only do it for a while – until your reserves start to run out (or, more accurately, start to approach the levels that schemes are required to hold as a safety buffer). For some open medical schemes, that time is now approaching. The losses must be brought to a halt so that those schemes can get back to a position that is sustainable in the long term. The practice of under-pricing to give reserves back to members is sometimes referred to as a “contribution holiday” because, just like real holiday, it cannot last forever. What goes down, must unfortunately come back up again.

Covid is behind us, and normality must return.

And so we find ourselves in the present benefit design and pricing climate where many medical schemes must return their contributions to levels that are commensurate with claims and expenditure. Viewed in isolation, the increases due to be announced by these schemes will appear to be high.

But these should be seen for what they are – the end of a deliberate process to move reserves back from the scheme into the hands of members, after which contributions must, unfortunately, return back to sustainable levels.

Get an email whenever we publish a new thought piece

Meet our experts

Author

More Insights

Focused Thought Pieces