UK Solvency II reforms: A balancing act

22 June 2022

14.7 min read

By Insight.

This is the first in a series of articles in which we will analyse the proposed reforms to the UK Solvency II regulations. This article summarises the proposed reforms, their expected benefits, and the impact on various stakeholders. Our next piece will be a more in-depth review of the impact of the reforms on annuity writers.

Our next piece will be a more in-depth review of the impact of the reforms on annuity writers.

In September 2021, the European Commission adopted a proposal for a comprehensive review of the EU Solvency II Directive. The UK government and the Prudential Regulation Authority (PRA) are following suit by undertaking their own review. They are currently seeking views on reforming the prudential regulatory regime for UK insurance firms (Solvency II) in a consultation closing on Thursday, 21 July 2022.

HM Treasury’s April 2022 Review of Solvency II: Consultation document details the government’s package of proposed reforms and invites all interested stakeholders to share their views on it.

The Review: Why and what

As outlined by the Treasury, “(t)he review is underpinned by three objectives:

- to spur a vibrant, innovative, and internationally competitive insurance sector

- to protect policyholders and ensure the safety and soundness of firms

- to support insurance firms to provide long-term capital to support growth, including investment in infrastructure, venture capital and growth equity, and other long-term productive assets, as well as investment consistent with the government’s climate change objectives.” 1

There is an inherent conflict in the above objectives: the desire to encourage growth and innovation while maintaining a level of prudence that will protect and ensure the financial soundness of firms. The PRA recognises that “(c)ombinations of reforms which reduce overall capital levels from their starting position will inevitably lead to some reduction in financial resilience, and this is directly relevant to the PRA’s statutory objectives for safety and soundness and policyholder protection. If liability values are below market transfer values, the risk of an insurer failure being disorderly would also increase. Assessing the quantum of these effects is inherently challenging.” 2

UK insurers realising benefits from the more favourable proposed reforms will still need to maintain the financial strength required to pay policyholders’ claims, with

the key test of capital adequacy being that an insurer would be able to transfer its business to another insurer

in a time of distress.

The proposed reforms to the regulation are, in short:

- a substantial reduction in the risk margin of around 60-70% for long-term life insurers;

- a reassessment of the fundamental spread used in the calculation of the matching adjustment;

- the introduction of a significant increase in flexibility to allow more investment in long-term assets; and

- a major reduction in the EU-derived regulations, which make up the current reporting and administrative burden.

Some of the reforms may have offsetting effects, with the overall impact being influenced by individual firms’ structures, mix of business and modelling choices. In particular, the benefits derived by insurers from reforms 1, 3 and 4 above may be offset by the increase in liabilities resulting from reform 2.

There are also interactions between various reforms, which means that they cannot be considered in isolation. For example, complex interdependencies exist between the risk margin and the fundamental spread, and both affect the liability value and the level of risk capital held by insurers. These two reforms would therefore need to be considered together.

The Reforms in More Detail

The Consultation document explains and poses questions for stakeholders on the proposed reforms. Each reform, as well as the rationale behind it, is outlined below.

1. Risk Margin: a modified cost of capital approach to reduce risk margin

The government is proposing a reduction in the size and volatility of the risk margin by using a modified cost of capital methodology. Decreases of up to 60%-70% for longterm life insurers and 30% for general insurers are on the cards.

The reform could manifest as an amendment to the cost-of-capital rate used in the risk margin formula. In addition, a new tapering parameter, lambda, could be introduced to allow progressively lower weight to be given to each year of projected future capital requirements.

While the government prefers the modified cost-of-capital approach, the Margin over Current Estimate model used in the Insurance Capital Standard set by the International Association of Insurance Supervisors is also being considered as a means to reduce risk margin.

Rationale for introducing a reduced risk margin:

- Additional capital resource on and reduced volatility of balance sheets: current risk margin methodology is sensitive to movements in interest rates, particularly when interest rates are low. It also moves in a procyclical manner. A reduction in the risk margin will reduce the volatility and associated procyclical behaviour of insurers’ balance sheets.

- Increased incentive for insurers to write new business and increase the affordability and range of their products due to the reduced volatility on their balance sheets.

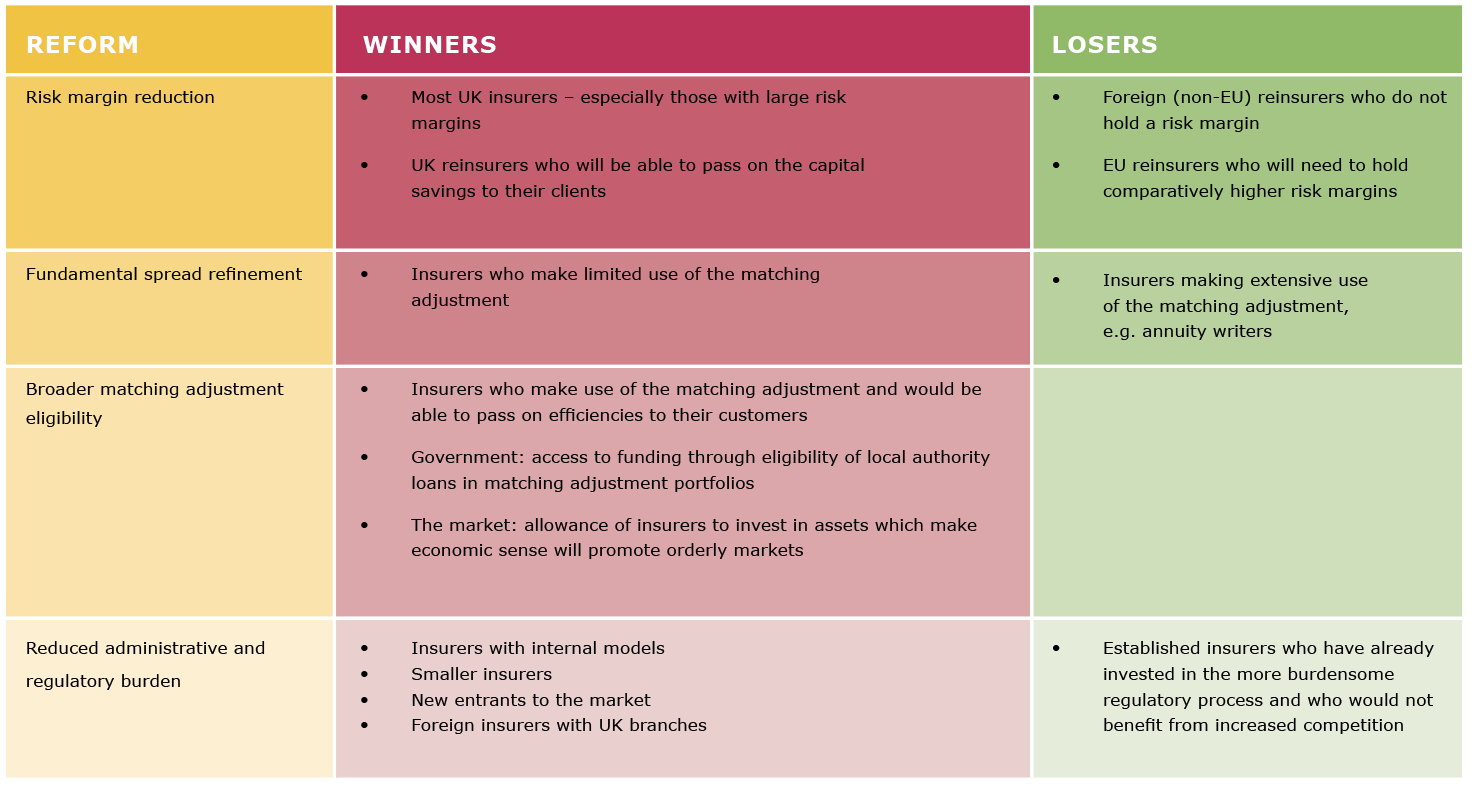

- Reduced incentive to reinsure outside the UK where a large risk margin is not required: currently, reinsurers based in jurisdictions where they are not required to hold a risk margin are popular among UK insurers because they can charge lower premiums. A smaller risk margin would allow UK reinsurers to offer lower rates, allowing them to compete with their foreign counterparts and potentially become attractive compared to reinsurers in the EU, where higher risk margins would still be required. The retention and attraction of reinsurance premiums in the UK would boost the UK economy

2. Matching Adjustment: ensuring the fundamental spread properly captures retained risks

Several indicators suggest that the current calibration of the fundamental spread does not capture the credit and other residual risks to which insurers are exposed. This has led to a desire to reform the fundamental spread, but there is not yet consensus on how it should be done. The reform is, however, likely to lead to a re-evaluation of internal models, especially those used by larger annuity writers, to determine the solvency capital requirement and will potentially incorporate market measures of credit risk.

Rationale for a reformed fundamental spread:

- Better understanding of insurers’ true risk exposure to assets and hence improved responsiveness to changes in investment decisions.

- More accurate reflection of long-term exposure to credit risk.

Recap of…

Matching Adjustment (MA)

Solvency II’s MA allows the insurer, under certain conditions, to increase the discount rate used to calculate technical provisions by an adjustment above risk-free, hence reducing its liabilities.

The trade-off of this benefit is that these insurers are required to hold a larger SCR.

Fundamental Spread (FS)

The adjustment to the discount rate mentioned above must be reduced by a prescribed haircut representing the “fundamental spread” for the MA assets. The FS accounts for the residual risks (like credit risk) retained by the insurer investing in these long-term assets even when illiquidity risk exposure is reduced.

3. Broader and Faster Matching Adjustment Eligibility: wider asset and liability eligibility and acceleration of eligibility decisions

The consultation proposes changes related to the matching adjustment, specifically around the assets and liabilities that are eligible for consideration. Specifically, the proposed reforms related to the matching adjustment are:

-

- Allowance of a wider variety of assets in matching adjustment portfolios, e.g. commercial real estate lending, local authority loan portfolios, infrastructure assets and callable bonds.

- Policyholder protection would be maintained through adequate risk mitigation techniques.

- Extension of the range of liabilities eligible for the matching adjustment. These liabilities include income protection products, as well as with-profits and deferred annuities. These products share similar economic characteristics to annuities and including them in the list of products eligible for the matching adjustment could reduce regulatory costs, which may lead to lower premiums for consumers.

- Encouragement of orderly markets:

- The removal of the disproportionately severe treatment of assets in matching adjustment portfolios whose ratings are below BBB would allow insurers to hold these assets rather than being forced to sell them.

- The introduction of a more proportionate approach to matching adjustment breaches would allow insurers to plan on the basis of a more stable matching adjustment benefit. It would also reduce costs associated with the loss of the matching adjustment benefit in the case of a breach.

- Introduction of a more streamlined approach to accelerate the review of matching adjustment eligibility applications for less complex assets.

- Efforts will be made to more rapidly evaluate matching adjustment applications for innovative assets whose risks may be difficult to assess, e.g. those with limited historical data.

Rationale for widening matching adjustment eligibility criteria:

- Annuity-writers are significant investors in bonds in the UK. Callable bonds are a popular form of debt in capital markets. Including callable bonds as eligible assets would likely increase the market depth and prices for callable bonds, which could stimulate further economic growth.

- Alignment of economic and regulatory outcomes by giving insurers the regulatory freedom to invest in assets which match their liabilities.

- Potential to invest in innovative assets and economic infrastructure, such as clean energy, transport, digital, water and waste, hence supporting the transition to net-zero.

- Ability to provide lower prices to consumers because of lower regulatory costs.

4. Reduced Reporting and Administrative Burdens: simplify the internal model framework and remove barriers to entry

The government has recognised that various improvements could be made to ease the administrative administrative burden on insurers from smaller new entrants to established internal model firms. The proposed reforms aimed at reducing reporting and administrative burdens include:

-

- Administrative and Reporting Efficiencies

- Reforms to the internal model framework, reducing the number and prescriptiveness of internal model standards requirements.

- Reforming reporting requirements by reviewing the appropriateness of current templates.

- Simplifying the calculation of Solvency II transitional measures on technical provisions.

- Capital Requirements

- Removal of requirements for branches of foreign insurers to calculate local capital requirements and hold local assets to cover them.

- Allowing more than one approach to the calculation of group capital requirements in certain circumstances.

- Increased Competition

- Increasing the thresholds before Solvency II applies to enable entry of smaller firms to the market.

- Introducing a mobilisation regime for new insurers by modifying entry requirements.

- Administrative and Reporting Efficiencies

Rationale for reducing reporting and administrative burdens:

- Enhanced UK attractiveness to foreign insurers.

- Increased competition should see new entrants and potential innovations in the market, benefiting consumers.

- Enablement of industry consolidation as groups are allowed to temporarily use multiple group internal models following an acquisition or merger.

Expected impacts

The precise impact will vary as proposed calibrations are finalised, but the PRA currently assesses, based on a risk margin reduction of 60% and a minimum recommended allowance for credit risk in the fundamental spread, that between 10% and 15% of capital would be released from the life sector in current economic conditions.3

Naturally, the proposed reforms will affect and benefit some insurers more than others, depending on the balance of good news and less favourable changes.

The reforms may be met with some resistance, for example, by insurers making extensive use of the matching adjustment (e.g. annuity writers), those that have operations in the EU (and want to retain equivalence with the European Solvency II regime) and the incumbents who stand to lose from a higher level of competition.

On the other hand, those that may welcome the reforms are smaller firms or new entrants to the market, foreign insurers operating in the UK and those with internal models.

Winners and Losers – who stands to benefit from the proposed reforms

UK insurers with an EU presence, i.e. those seeking to maintain equivalence with European Solvency II, will likely be disadvantaged by all of the proposed reforms. These insurers may need to maintain two sets of bases, and absorb the associated increased regulatory and administrative burdens.

Remembering the policyholder

Insurers are advised to actively participate in the consultation to ensure that their views and concerns are heard. Ultimately, however, the overarching objective of Solvency II – to protect policyholders – should not be forgotten. This sentiment is reflected in a statement from IFoA President, Louise Pryor:

“Any redesign of Solvency II to ensure ‘Solvency UK’ is fit for today’s current and emerging challenges needs to be a careful balance of the four factors set

out by the government.

The IFoA believes this mix is essential to deliver what is in the wider public interest, given the great potential of insurance investment in both levelling up and creating a more sustainable, green economy. However, this innovation needs to be balanced with the consumer and policyholder protection.”

This has been the first in a series of articles in which we analyse the proposed reforms to the UK Solvency II regime. Please keep an eye out for our next piece, in which we will consider in more detail the impact of the reforms on annuity writers. Insight has significant experience in assisting insurers in dealing with regulatory change. Please be in touch should you wish to discuss the impacts of the proposed reforms on your business.

View or download the PDF here

insight.co.za | lifesolutions@insight.co.za

[1] Source: UK government website

[2] Source: PRA’s DP2/22 – Potential Reforms to Risk Margin and Matching Adjustment within Solvency II

[3] Source: PRA’s DP2/22 – Potential Reforms to Risk Margin and Matching Adjustment within Solvency II

Get an email whenever we publish a new thought piece

In 2023, Insight Life Solutions conducted a series of surveys to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the progress made

3.2 min read

Insight Life Solutions conducted a series of five surveys in Q3 2022 to seek South African life insurers’ views on specific IFRS 17 topics. The surveys aimed to summarise the

3.5 min read

Meet our experts

Author

More Insights

Focused Thought Pieces